Asset-Based Long Term Care: Protect Your Assets and Secure Your Future

Posted in Long Term Care Insurance last updated on May 6, 2026

Posted in Long Term Care Insurance last updated on May 6, 2026Estimated reading time: 9 minutes

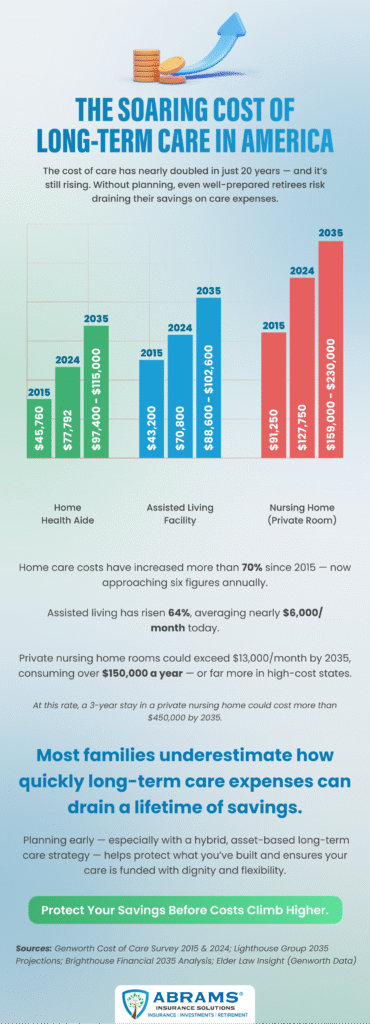

Long-term care expenses are rising faster than most retirees anticipate, especially when it comes to home health care. With rates often ranging from $30 to $40 an hour, the cost of having help at home just eight hours a day, seven days a week can easily reach $10,000 a month—over $120,000 a year. Many families are surprised to learn that staying at home can be just as expensive as facility care. As Americans live longer and prefer to age in place, these rising costs can quickly erode retirement savings meant to last decades.

Quick Answer

Asset-based long term care (LTC) insurance is a hybrid policy that combines long-term care coverage with a life insurance or annuity component. It allows you to use your policy’s value to pay for care if needed. And, perhaps more importantly, if you never require care, your heirs receive a death benefit, or you retain access to cash value. This makes it a flexible way to protect your assets and secure your future while ensuring your money always provides value.

What is traditional long term care insurance? Learn what long term care is and how to pay for it. Pass along LTC risk to an insurance company and protect your retirement.

Table of contents

- The Harsh Reality of Long-Term Care Expenses

- What Is Asset-Based Long-Term Care Insurance?

- Key Advantages of Asset-Based Long-Term Care Policies

- How Asset-Based LTC Benefits Are Triggered and Delivered

- Funding Your Asset-Based LTC Policy: Strategies and Options

- Conclusion: Securing Your Peace of Mind with Asset-Based Long-Term Care

The Harsh Reality of Long-Term Care Expenses

Many families underestimate the true financial impact of long-term care. Medicare covers little to none of these costs, leaving individuals and their families to shoulder the burden. Without a plan, even well-funded retirees risk draining their assets, impacting both their lifestyle and legacy.

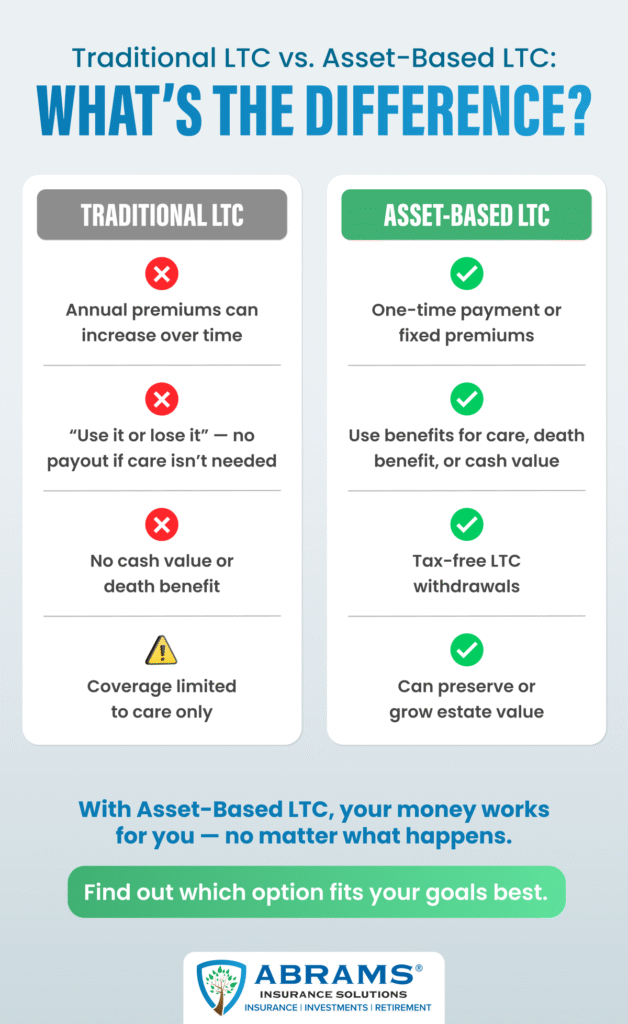

Traditional long-term care insurance once seemed like the obvious answer. But it comes with drawbacks—rising premiums, potential rate increases, and the dreaded “use it or lose it” risk. If you never need care, those premiums are gone forever. These new pressures on everyday people have pushed the industry into creating a more flexible solution.

Understanding Asset-Based Long-Term Care: A Modern Hybrid Solution

Asset-based long term care insurance is a flexible solution that blends traditional insurance products with a long-term care rider. Instead of paying ongoing premiums for a standalone policy, you typically invest a lump sum into a hybrid life insurance or annuity plan. This creates a pool of funds that can be used in multiple ways—either for long-term care costs, a death benefit for loved ones, or a return of premium if you change your mind. Because every person’s financial planning needs are unique, these policies can be tailored to cover different types of long-term care, such as home health aides, assisted living, or nursing facilities. While these policies can be advantageous, always seek qualified tax advice before purchasing, as the details of benefits and withdrawals can vary based on your individual situation.

What Is Asset-Based Long-Term Care Insurance?

Asset-based long term care insurance is designed to help you plan for future care needs without wasting money if you never use it. These policies typically involve a one-time premium or limited-pay option. In exchange, you receive both long-term care protection and a life insurance or annuity component that ensures your money always benefits you or your beneficiaries.

The Core Difference: How It Compares to Traditional LTC Insurance

When comparing asset based vs traditional long term care, the differences are significant:

| Feature | Asset-Based LTC | Traditional LTC |

|---|---|---|

| Premium Increases | Fixed or single pay | Can increase over time |

| Use It or Lose It | No – death benefit or cash value remains | Yes – benefits lost if unused |

| Benefit Type | LTC + life insurance or annuity | LTC only |

| Tax Advantages | Tax-free LTC benefits | Tax-free LTC benefits |

| Estate Value | Can preserve or grow | None |

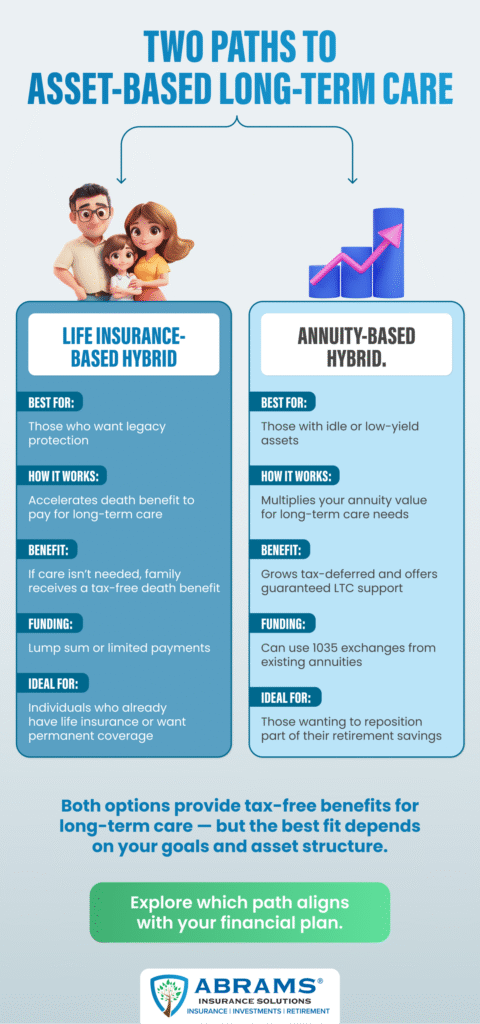

The Two Main Structures of Asset-Based Long-Term Care

Life Insurance-Based Hybrid Policies

These policies allow you to accelerate your death benefit to pay for long-term care expenses, helping you manage healthcare costs without draining savings. Rather than paying annual premiums indefinitely, you fund the policy once or over a set period, giving you predictable costs. This approach balances your financial needs with the rising cost of long-term care while protecting your legacy.

For example, a retiree who deposits $100,000 into an asset-based policy might receive up to $300,000 in long-term care benefits. If care isn’t needed, the remaining value becomes a tax-free death benefit for heirs.

Actual benefits and performance vary by carrier, product design, underwriting approval, and state regulation. Policy illustrations are not guarantees of future results.

Annuity-Based Hybrid Policies

Annuity-based options multiply the value of your investment when used for long-term care, providing significant leverage when a long-term care event occurs. These products combine the financial strength of an annuity with the protective features of long-term care coverage, allowing you to turn underperforming funds into guaranteed support for future long-term care services. They can be ideal for repositioning low-yield assets into tax-advantaged coverage. At the same time, hybrid policies can offer stable growth and security similar to permanent life insurance.

For example, an individual might transfer $150,000 from a traditional savings account into an annuity-based hybrid policy. If they later require long-term care services such as home health aides or assisted living, their benefit pool could grow to $450,000 or more, providing a reliable source of funding for care while preserving their remaining assets for other financial goals.

For annuity-based hybrid products, growth, bonuses, and LTC multipliers vary by product and are not guaranteed unless explicitly stated in the contract.

Choosing the Right Structure: Life-Based vs. Annuity-Based

The right structure depends on your goals. Life-based hybrids tend to appeal to those seeking legacy protection, while annuity-based plans suit those with taxable deferred assets they wish to reposition. Your advisor can help you match the right fit to your overall financial plan.

Key Advantages of Asset-Based Long-Term Care Policies

- Eliminating the “Use It or Lose It” Dilemma – You get value either way: through LTC benefits, a death benefit, or accessible cash value.

- Asset Protection and Legacy Preservation – Protects your wealth while still allowing a legacy for loved ones.

- Significant Potential Tax Advantages and Efficiencies – Withdrawals for qualified long-term care expenses are generally tax-free under federal law.

- Flexibility, Customization, and Growth Potential – Choose benefit amounts, inflation protection, and premium structures that fit your goals.

How Asset-Based LTC Benefits Are Triggered and Delivered

- Qualification for Benefits: Meeting Chronic Illness Criteria – Benefits typically activate when you cannot perform two of six Activities of Daily Living (ADLs) or have severe cognitive impairment.

- Comprehensive Coverage: A Broad Spectrum of Care Services – Coverage can include home health care, assisted living, adult day care, hospice, and skilled nursing facilities.

- Value-Added Services: Beyond Financial Benefit – Many policies include care coordination, wellness resources, and family support programs.

Funding Your Asset-Based LTC Policy: Strategies and Options

Understanding Premium Payments and Structures

You can fund your policy with a single premium or pay over several years. Once funded, your benefits are guaranteed.

Leveraging Existing Assets: Advanced Funding Strategies

You may use underperforming savings, CDs, or 1035 exchanges from existing life insurance or annuity contracts—allowing you to reposition idle assets efficiently.

Important Considerations and Potential Trade-Offs

Cost comparison: asset-based vs. traditional LTC insurance. Asset-based policies often require a higher upfront cost but offer guaranteed benefits, predictable premiums, and multiple payout options.

The underwriting process and eligibility requirements. Medical underwriting is often simpler than with traditional LTC, focusing on overall health and functionality.

Understanding surrender charges and access to cash value. Some policies include surrender periods. Always review liquidity options before committing.

Integrating Asset-Based LTC into Your Broader Financial Plan

A foundational pillar of retirement security. Asset-based LTC helps secure your retirement income by preventing unplanned care costs from derailing your financial future.

Complement other planning strategies. It pairs well with annuities, life insurance, and tax-advantaged income strategies.

Tailor coverage to your unique needs and goals. Every policy can be customized to balance protection, flexibility, and legacy preservation.

Pros and Cons of Asset-Based Long-Term Care Insurance

Pros:

- Guaranteed benefits (LTC, death benefit, or cash value)

- No rate increases

- Tax-free LTC withdrawals

- Simplified underwriting

- Legacy protection for heirs

Cons:

- Higher upfront premium

- Limited liquidity during the early years

- May not suit individuals with minimal assets

Next Steps: Making an Informed Decision for Your Future

The Indispensable Role of Expert Guidance

Choosing the right policy requires experience and access to multiple carriers. Independent advisors can compare dozens of plans to ensure your money works efficiently.

Key Questions to Ask

- What’s the best structure for my financial goals?

- How can I fund the policy most efficiently?

- What are my liquidity options?

- How do benefits interact with other policies I own?

Side note: If you really want to get specific about how much long-term care you may need in your area, check out the Genworth Cost of Care Study.

When shopping for long term care insurance, it’s important to understand what long term care insurance covers. Learn the lingo and what to look for in your policy.

Conclusion: Securing Your Peace of Mind with Asset-Based Long-Term Care

Asset-based long term care is more than insurance—it’s a strategy. It provides financial flexibility, preserves wealth, and ensures that whether you need care or not, your investment works for you.

These policies are built to respond when a long-term care need arises, offering access to funds for medical care or assistance with daily activities. They let you select the amount of coverage that fits your retirement account balance, your type of long-term care preference, and your desire to leave a financial legacy for loved ones. By preparing ahead, you can reduce the emotional and financial burden on family members while maintaining control and dignity during a time when care is most needed.

How Abrams Insurance Solutions Can Help

At Abrams Insurance Solutions, we help clients nationwide protect their assets and prepare for life’s uncertainties. Our fiduciary approach ensures your long-term care plan aligns with your broader retirement goals. We compare top-rated companies and tailor policies to your specific needs.

Ready to explore your options? Schedule a consultation at (858) 703-6178 or click the link below to get started.