Disability insurance for maternity leave can help replace a portion of your income while you recover from childbirth, but it typically does not cover routine maternity leave or bonding time. Most policies only pay benefits when pregnancy, childbirth, or a related medical condition prevents you from working. To qualify, coverage usually must be in place before you become pregnant, and many policies include waiting periods or pre-existing condition limitations. After eligibility requirements are met, short-term disability insurance can provide income replacement during your physician-certified recovery period after childbirth.

Key Takeaways

Most short-term disability policies do not cover routine maternity leave.

Benefits are typically limited to the medical recovery period after childbirth.

Coverage generally must be in force before pregnancy begins.

A normal delivery may qualify for benefits if policy requirements are met.

Pregnancy complications may qualify for additional disability benefits.

Short-term disability pays income replacement, not medical bills.

Your paycheck doesn’t pause when you give birth. But in the U.S., paid maternity leave is far from guaranteed. According to the U.S. Bureau of Labor Statistics, only 27% of civil and private-sector workers have access to employer-paid family leave, leaving the majority of women to figure out how to replace their income on their own.

Short-term disability insurance can be one way to replace a portion of your income during a qualifying maternity-related disability. But whether it actually pays during maternity leave depends on three things: the type of policy you have, when you enrolled, and the circumstances of your pregnancy and delivery.

If you have short-term disability through your employer, you may already have coverage since most group plans include pregnancy recovery benefits if you were enrolled before becoming pregnant. If you’re self-employed, a freelancer, or your employer doesn’t offer disability benefits, individual policies like Illinois Mutual’s SIDI can fill that gap, but timing is everything, and the window to act is before conception, not after a positive test.

This guide breaks down exactly how short-term disability works for maternity leave, what it covers, what it doesn’t, and how to structure your coverage so it actually pays when you need it most.

What Is Short-Term Disability Insurance and How Does It Relate to Pregnancy?

Short-term disability insurance for maternity leave is a type of coverage that replaces a portion of your income when pregnancy, childbirth, or related medical conditions prevent you from working. Unlike health insurance, which pays medical bills, disability insurance pays you directly so you can cover everyday expenses like rent, groceries, and utilities during recovery.

Does Short-Term Disability Insurance Actually Cover Maternity Leave?

Usually no. Most short-term disability policies cover medical conditions rather than routine maternity leave or bonding time. Still, some policies allow childbirth to qualify as a medical event if you satisfy certain eligibility and timing rules.

This distinction is really important to understand. Disability insurance covers your physical recovery, not elective time off after your doctor clears you to return to work.

Why Most Disability Insurance Doesn’t Cover Maternity Leave

Disability insurance centers on one core requirement: a covered sickness or injury must prevent you from working.

Routine maternity leave typically fails to meet this definition. Insurers do not classify pregnancy as a disability unless medical complications or childbirth recovery physically stop you from doing your job.

Because of this, many employer plans and individual policies offer little to no income replacement, even when policyholders expect coverage.

Where Disability Insurance Can Apply to Maternity Leave

While most policies don’t cover routine leave, disability insurance can still play a critical role in maternity planning when structured correctly.

Coverage may apply in situations such as:

Recovery from childbirth (vaginal or C-section)

Pregnancy complications requiring bed rest or extended recovery

Medically documented inability to perform job duties

This is where certain individual policies, including Illinois Mutual simplified issue, can provide meaningful income protection when the timing and eligibility requirements are met.

What If You Already Have Short-Term Disability Through Your Employer?

If your employer offers group short-term disability coverage, your situation is different from that of someone buying an individual policy. Employer group plans typically don’t require medical underwriting, which means you won’t be turned down for a pre-existing condition the way you might with an individual policy, and in many cases, pregnancy is a covered condition from the moment your enrollment is active.

Under most group plans, you can expect 50–70% income replacement for approximately six weeks after a vaginal delivery and eight weeks after a C-section, subject to your plan’s elimination period and benefit terms. Complications may extend that window.

If you have employer coverage, your key steps are to confirm with HR that pregnancy is covered under your specific plan, figure out if your PTO can bridge the elimination period, and learn how to file your claim well before your due date.

Where individual policies like Illinois Mutual’s SIDI become relevant is when your employer plan has a coverage cap, doesn’t exist at all, or you’re self-employed, in which case SIDI fills the gap your group plan leaves behind.

What Makes Illinois Mutual’s SIDI Policy Different for Maternity Coverage?

Illinois Mutual’s SIDI policy is a Voluntary Short-Term Disability Income Policy. You purchase this policy as an individual; it belongs to you personally (not your employer), and it stays with you regardless of where you work. It’s guaranteed renewable until age 72, so once you’re approved, the carrier cannot cancel your coverage as long as you pay your premiums.

With an Illinois Mutual SIDI policy, having a baby is treated like any other medical “sickness.” To qualify for benefits, your policy must have been active for at least nine consecutive months before the delivery date, and the pregnancy cannot be considered a pre-existing condition.

When these timing requirements are met, the insurance serves as a functional income-protection plan rather than a theoretical benefit. In most cases, Illinois Mutual provides approximately six weeks of coverage for a vaginal delivery and eight weeks for a C-section. Additionally, policies for Virginia residents may provide at least 12 weeks of coverage for a normal pregnancy.

It is also equally important to understand what this benefit covers and what it does not. The SIDI policy covers your physical recovery from childbirth, not elective bonding time or parental leave beyond your physician-certified recovery period. The benefit window ends when your doctor clears you to return to work, not when your FMLA leave expires.

Key Features of Illinois Mutual’s SIDI Policy

Simplified application process

The policy uses a fully electronic application process. No physical exam, no lengthy paperwork.

Because of the simplified issue approach, approvals happen much faster than traditional DI underwriting, which is particularly important when you’re working against a timing window before conception.

24-hour coverage

Coverage applies both on and off the job. This is critical for maternity-related claims, since pregnancy disability occurs entirely outside of working hours. Workers’ compensation provides no protection here. SIDI does.

Guaranteed renewable to age 72

Once your policy is issued, it’s yours to keep until age 72, as long as you pay your premiums. This means it protects your paycheck far beyond maternity leave. Think of it as the foundation of your wealth-building strategy. By securing your income now, you ensure that an unexpected illness or injury won’t derail your ability to fund high-level plans like Kai-Zen or your tax-free retirement accounts.

Unisex and uni-tobacco rates

Premium rates do not vary based on gender or tobacco use. Women are not charged more than men for the same coverage. This is a meaningful distinction in a market where individual disability policies often price women higher.

What Is the 9-Month Rule and Why Does It Make or Break Your Coverage?

The 9-month rule changes everything for women who plan ahead, and it catches them off guard when they wait.

The SIDI policy language is clear: normal pregnancy is not covered if it occurs within the first nine months after the policy’s effective date. In addition to satisfying the nine-month threshold, the disability must not fall under the policy’s pre-existing condition limitations, which exclude conditions diagnosed, treated, or symptomatic within 12 months before the date of issue during the policy’s first year in force.

Purchase your policy before you conceive. The nine-month clock starts on your policy’s effective date, and it must expire before your delivery date for maternity benefits to apply.

If You Are Already Pregnant

If your policy has not been in force for at least nine full months before your delivery date, normal pregnancy benefits will not apply to this pregnancy. Contact Abrams Insurance immediately to evaluate your specific situation, review your state’s paid leave options, and maximize your available coverage for this birth.

The only exception to this timing framework is that pregnancy complications are treated like any other illness under the policy and are not subject to the nine-month requirement for a normal pregnancy…. More on this in the next section.

How Much Can Short-Term Disability Actually Pay You During Maternity Leave?

Disability insurance is not just about income replacement in theory. It’s about keeping your financial life stable while you recover.

Monthly Benefit Amounts

The Illinois Mutual SIDI policy typically provides:

Up to 60% of your monthly income

Maximum benefit of around $3,000 per month

Your benefit amount depends on your income. You can purchase up to 60% of your monthly pay, capped at $3,000. Please note that your total coverage from all insurance sources cannot exceed this $3,000 limit.

Benefit Calculation Example

It is important to understand that your elimination period is part of the standard recovery window, not an addition to it. If your doctor certifies a 6-week recovery for a vaginal delivery and you have a 7-day elimination period:

Total Disability Window: 6 Weeks

Elimination Period (Unpaid): 1 Week

Actual Payout Period: 5 Weeks

If you earn $60,000 per year and qualify for a $3,000 monthly benefit, you would receive approximately $3,461 for a 5-week payout (vaginal) or $4,846 for a 7-week payout (C-section). These benefits are generally received tax-free because you paid the premiums with after-tax dollars.

Everyday Expenses It Helps Cover

The benefit is designed to cover real life, not just a line item in a financial plan. During your maternity recovery, SIDI benefits can go directly toward your mortgage or rent, utilities, groceries, and other essential monthly bills. That’s what makes this a practical financial strategy rather than a theoretical one.

Since you pay SIDI premiums with after-tax dollars, you generally receive your benefits tax-free. This is a meaningful advantage that raises the effective income replacement rate above what the percentage alone suggests. Consult our specialist for guidance specific to your situation.

What Happens If You Have Pregnancy Complications?

Illinois Mutual’s SIDI policy covers pregnancy complications just like any other sickness. They are not subject to the nine-month normal pregnancy waiting period.

Examples of covered pregnancy complications that could prevent you from working include:

Medically ordered bed rest, preeclampsia, hyperemesis gravidarum, and gestational diabetes. This also extends to any other physician-documented condition that prevents you from performing your essential job duties before or after delivery.

If complications keep you from working longer than the standard 5 to 7 weeks, Illinois Mutual will review your doctor’s notes to see if you qualify for more benefits. Your doctor’s specific documentation of why you cannot work is the most important part of your claim. It’s best to keep thorough records and maintain consistent communication with your OB-GYN or treating provider throughout your recovery.

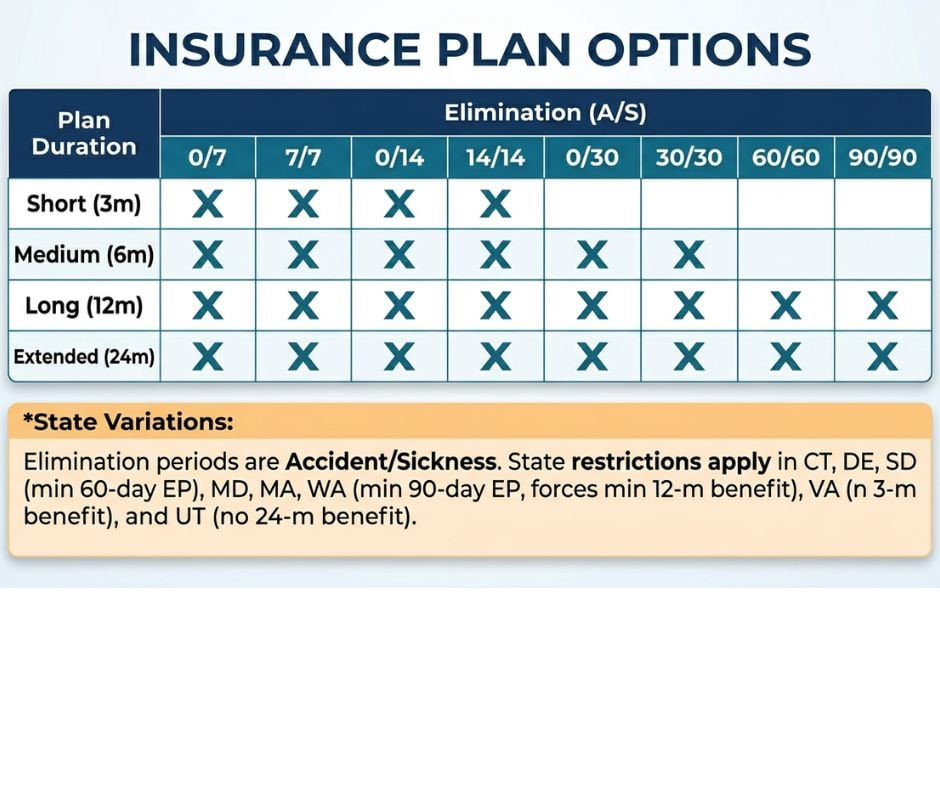

How Do Elimination Periods Work for Maternity Claims? (This Catches Most People Off Guard)

Even with active coverage, your specific policy structure controls the timing and method of your payouts.

Elimination Period (Waiting Period)

The elimination period is the number of continuous days you must be totally disabled before benefits begin to accrue and become payable. Think of it as a time-based deductible; shorter means benefits begin sooner but premiums are higher; longer means lower premiums but a gap period you cover yourself.

CRITICAL NOTE: For maternity claims, the elimination period is part of the 6- or 8-week recovery window. It is not added to the end. For example, if you have a 6-week recovery window and a 7-day elimination period, you will receive payments for 5 weeks.

Why this matters for your strategy:

For the 6-week vaginal delivery recovery: If you choose a 30-day elimination period, your payout will only be about 2 weeks.

Recommendation: To maximize your maternity check, a 7-day or 14-day sickness elimination period is usually the most effective choice, even though the premium is slightly higher.

How Does Short-Term Disability Work Alongside FMLA and Your Paid Time Off?

Most working women navigate a layered system of overlapping protections during maternity leave. Understanding how they fit together helps close income gaps and maximize your total leave benefit.

Elimination period – bridge with PTO or sick leave

SIDI benefits begin after your chosen elimination period expires. Use accrued PTO or sick leave during this window to keep income flowing from day one.

SIDI benefits begin – run concurrently with FMLA

After you meet the elimination period, your SIDI policy pays your monthly benefit. While FMLA protects your job, it provides zero pay; SIDI steps in to fill that income gap for eligible employees.

Physician certifies your recovery window

Your OB-GYN or treating physician certifies your recovery period. SIDI continues paying through your authorized window, which can be 5 weeks, 7 weeks, or longer if complications are documented.

SIDI ends – remaining leave on your terms

After medical recovery, SIDI ends. Any remaining FMLA leave, state-paid family leave (where available), or employer bonding leave extends your time before returning to work.

If your employer also provides a group short-term disability plan, coordinate carefully. Illinois Mutual’s SIDI participation limit caps combined disability benefits from all sources at $3,000 per month, so layering policies strategically, rather than duplicating coverage, is the right approach.

Common Misconceptions About Disability Insurance for Maternity Leave

“All disability insurance covers maternity leave.”- This is one of the most expensive misconceptions in personal finance. Many disability policies, especially employer group plans, have specific exclusions, waiting periods, or definitions that limit or eliminate maternity benefits. Coverage must be verified policy by policy. Never assume.

“If pregnancy is covered, leave is covered.” – Coverage depends on policy definitions, waiting periods, and whether the situation meets the definition of disability. SIDI covers your physical recovery from childbirth. It does not cover elective leave beyond your physician-authorized recovery window, bonding time, or time off you choose to take after being medically cleared.

“Workers’ compensation would cover this.” – Workers’ compensation only applies to work-related injuries or illnesses. Pregnancy is not covered under workers’ comp under any circumstances. SIDI provides 24-hour off-job coverage specifically designed to fill this gap.

“I can buy coverage after I get pregnant.”- The nine-month waiting period for a normal pregnancy and the pre-existing condition limitation make this approach ineffective for the current pregnancy in virtually all cases. The window to act is before conception, not after a positive test.

Is Short-Term Disability for Maternity Leave Right for You?

While this strategy is not a universal fit, it serves as a critical financial tool for specific individuals. For those who fall into the following categories, securing a policy can be the difference between a stressed leave and a focused one.

Women Planning for a Future Family

This is the most effective scenario for utilizing disability insurance. Because of the industry-standard nine-month waiting period for maternity benefits, the ideal time to establish coverage is well before pregnancy occurs. Taking action early ensures that you have access to income-protection options that are generally unavailable once a pregnancy is already underway.

Self-Employed Professionals and Business Owners

As an entrepreneur or freelancer, you are essentially your own HR department. Without the safety net of employer-sponsored group benefits, your personal income stops the moment you stop working. In this case, disability insurance isn’t just a perk; it is a vital business-continuity strategy that ensures your personal expenses are covered while you are away from your company.

Employees with Limited or No Paid Leave

Many traditional jobs offer protected time off through FMLA, but do not actually provide a paycheck during that time. If your employer offers little to no paid maternity leave, or if you have a limited amount of accrued PTO, disability insurance serves as the bridge that fills the financial gap. It allows you to focus on your recovery and your newborn without the immediate pressure of returning to work for a paycheck.

This Strategy Is NOT Ideal For

Women Who Are Already Pregnant

Because of the strict nine-month waiting period required for maternity benefits, this policy is not a viable solution for those who are currently pregnant. If the policy has not been in force for the required timeframe before delivery, benefits for a normal pregnancy will not apply.

Individuals Seeking Paid Bonding Leave

It is important to distinguish between medical disability and family leave. SIDI policy is specifically designed to cover a medical disability resulting from childbirth. It is not a paid family leave or “bonding leave” policy. If your goal is to receive a paycheck for voluntary time off to be with your newborn after your physical recovery is complete, this insurance will not fill that specific role.

Residents in Non-Participating States

While this coverage is a powerful tool, it is not available in every state. Availability must be confirmed upfront to ensure you are looking at a strategy that is legally accessible to you.

What Are Your Options If Short-Term Disability Won’t Cover Your Leave?

If you’re already pregnant, in a non-participating state, or simply looking to extend your leave beyond the physician-certified recovery window, there are several strategies worth building into your plan:

Bank your PTO early: Saving your sick days and vacation time gives you the best head start. Used strategically, they can cover your elimination period, supplement disability benefits, or extend your leave after SIDI ends.

Fund an HSA or FSA: Health Savings Accounts and Flexible Spending Accounts let you set aside pre-tax dollars for qualified medical expenses, including many maternity-related costs. An HSA has the added advantage of rolling over year to year, making it a reliable long-term savings vehicle for pregnancy planning.

Build a dedicated maternity savings fund: Even setting aside a modest amount each month before conception can create a meaningful financial cushion. Think of it as self-insuring the portion of your leave that no policy will cover.

Coordinate with your partner’s leave. If your partner has paid leave available, staggering your leave periods can extend the total window your family has coverage.

Questions to Ask Before Buying Disability Insurance for Maternity Leave

Before making any decision, these are the questions whose answers determine whether the policy actually works for your situation.

Does the policy cover normal pregnancy, complications, or both?

How long must you keep the policy in force before it covers pregnancy?

What is the elimination period, and how does it affect my maternity benefit?

How much of my income can the policy actually replace, and is there a monthly maximum?

How long will benefits last, and does this policy cover complications beyond the standard window?

Is this product available in my state, and are there state-specific benefit differences?

FAQs

Does disability insurance cover maternity leave?

Usually no. Most policies do not cover routine maternity leave, but some exceptions exist.

Q: Does the Pregnant Workers Fairness Act (PWFA) affect my disability coverage?

Not directly, but it’s worth knowing about. The PWFA requires employers with 15 or more employees to provide reasonable accommodations for pregnancy-related limitations, such as modified duties, extra break time, or a temporary schedule change. It doesn’t replace income the way disability insurance does, but accommodations under the PWFA can sometimes reduce the period where you’re fully unable to work

How long does my SIDI policy need to be in force before maternity benefits apply?

Nine full months. The policy must have been in force for at least nine months before your delivery date, and the disability must not fall under the pre-existing condition limitation.

Does SIDI policy cover a normal pregnancy?

Yes, after the policy has been in force for at least 9 months.

Does SIDI cover pregnancy complications, and are they subject to the 9-month rule?

Yes, and no. Pregnancy complications or other conditions that prevent you from working are covered as any other sickness under the SIDI policy. They are not subject to the nine-month normal pregnancy waiting period. If complications extend your recovery beyond the standard benefit window, Illinois Mutual reviews your physician’s documented restrictions to determine whether additional benefits are due.

Can I buy disability coverage while pregnant?

Consult our specialist immediately if you are already pregnant and uninsured. If the policy can be issued at least nine full months before your expected delivery date, the maternity provision could still apply. However, the pre-existing condition limitation and the timing of your pregnancy will both factor into whether this birth is covered.

How early should I apply for Disability Insurance for Maternity Leave?

Ideally, before pregnancy, to satisfy the waiting period requirements.

Does SIDI cover me if I’m self-employed or don’t have employer benefits?

Yes, for self-employed professionals and business owners, individually purchased disability income insurance, such as SIDI, is especially critical.

How We Can Help You Navigate This

Navigating disability income planning requires more than just picking a policy; it requires a strategy that evolves with your family planning journey. Whether you are a business owner in California or a professional in Virginia, our team provides the same high-level, nationwide expertise to secure your income.

At Abrams Insurance Solutions, we act as your advocate to ensure your coverage is functional, not just theoretical. We help you:

Understand what’s actually covered: We translate complex policy language into plain English, which means no assumptions, no surprises at claim time.

Compare options across multiple carriers: We’re not limited to one carrier. We find the policy structure that fits your income and timeline.

Structure policies around your timeline: Timing your purchase relative to your planned conception is everything. We build your plan specifically around your family goals.

Avoid costly waiting-period mistakes: Our team proactively flags pre-existing condition clauses and elimination-period pitfalls before they have a chance to cost you a claim.

If you are planning for a family, the decisions you make about when to buy and how to structure your coverage determine whether your policy actually pays when you need it most. We provide the expertise to help you get both right.

About Chris Abrams

I'm a life insurance and retirement planning specialist. My goal is to help my clients build wealth and save time and money when shopping for insurance. Learn strategies to build wealth with less risk, taxes and fees. Read our client reviews to learn what it is like to work with us. My team is licensed in all 50 states and represents over 70 insurance companies. If you have been declined for coverage, have a special need or have questions; contact us. We have creative solutions for almost every situation.

Posted in Disability Insurance last updated on July 6, 2026

Posted in Disability Insurance last updated on July 6, 2026