Qualified vs Non-Qualified Retirement Plans – What’s the Difference?

Posted in Indexed Universal Life (IUL) last updated on July 1, 2026

Posted in Indexed Universal Life (IUL) last updated on July 1, 2026Quick Answer: Qualified and non-qualified retirement plans differ in their tax treatment, contribution limits, employee eligibility requirements, and regulatory oversight. Qualified retirement plans such as 401(k)s, 403(b)s, SEP IRAs, SIMPLE IRAs, and pension plans must satisfy IRS and ERISA requirements. Non-qualified plans, such as deferred compensation plans, supplemental executive retirement plans (SERPs), and certain cash-value life insurance strategies, offer greater flexibility but fewer legal protections.

Key Takeaways

- Qualified retirement plans must comply with IRS and ERISA requirements.

- Common qualified plans include 401(k)s, 403(b)s, SEP IRAs, SIMPLE IRAs, and pension plans.

- Non-qualified plans often provide greater contribution flexibility.

- Qualified plans generally offer stronger creditor protections.

- Many high-income earners use both qualified and non-qualified retirement strategies.

- Indexed Universal Life insurance is not a qualified retirement plan but may serve as a supplemental retirement income strategy.

- Diversifying tax treatment across retirement assets may help improve retirement flexibility.

Table of Contents

- Key Takeaways

- What is a Qualified Retirement Plan?

- Types Of Qualified Retirement Plans

- Benefits of Qualified Plans

- Disadvantages of Qualified Retirement Plans

- What Is a Non-Qualified Retirement Plan?

- Types of Non-Qualified Plans

- Popular Wealth Building Strategies

- What is Indexed Universal Life Insurance?

- How Some People Use IUL as a Supplemental Retirement Strategy

- Potential Advantages of IUL

- Potential Drawbacks of IUL

- FAQs

- Qualified vs Non-Qualified Retirement Plans: Which Is Better?

Understanding the difference between qualified and non-qualified retirement plans is an important step in building a retirement strategy that aligns with your goals. While qualified plans such as 401(k)s and IRAs are often the foundation of retirement savings, they are not the only options available. Business owners, executives, and high-income professionals frequently explore non-qualified retirement plans and other supplemental strategies after maximizing their qualified plan contributions. Each approach offers unique advantages, limitations, tax considerations, and levels of flexibility.

In this guide, we’ll explain how qualified and non-qualified retirement plans work, compare their benefits and drawbacks, and discuss where Indexed Universal Life Insurance (IUL) may fit into a diversified retirement income strategy.

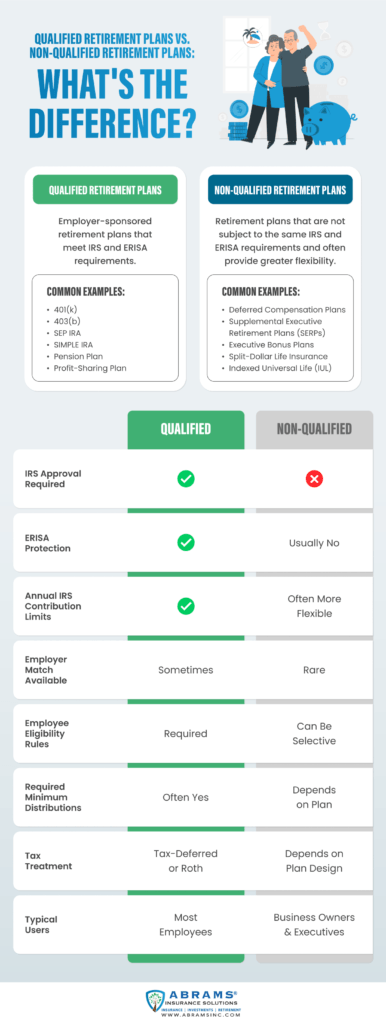

What is a Qualified Retirement Plan?

A qualified retirement plan is an employer-sponsored, structured savings program that provides retirement income to employees and their beneficiaries. These plans are designed to meet specific criteria outlined in the Internal Revenue Code (IRC) and adhere to the guidelines set forth by the Employee Retirement Income Security Act (ERISA).

The key characteristics of a qualified retirement plan include compliance with federal regulations on accountability, transparency, and equal access for all eligible employees.

Types Of Qualified Retirement Plans

Qualified retirement plans primarily fall into two categories: defined benefit and defined contribution. Additionally, there are hybrid options, like the cash balance plan.

Defined benefit plans provide employees with an assured payout upon retirement, shifting investment risk to the employer, which must save and invest adequately to fulfill the plan’s obligations. A traditional annuity-based pension is a classic example of a defined benefit plan.

In contrast, defined contribution plans are structured so that retirement income depends on the amounts employees choose to contribute and on the performance of those investments.

Employees typically can select their investment options and assume all associated risks. The 401(k) is a well-known example of a defined contribution plan.

Other examples of qualified plans include 403(b) plans, pension plans, profit-sharing plans, and Employee stock ownership plans (ESOPs)

Employers managing qualified retirement plans have specific responsibilities. They must ensure that the plans are operated in accordance with the established guidelines and provide clear information to plan participants about their benefits.

Furthermore, employers must be vigilant about changes in retirement plan laws and regulations to maintain their plans’ qualified status. This commitment not only protects employees’ interests but also ensures that both employers and employees can fully benefit from the tax advantages associated with qualified retirement plans.

Benefits of Qualified Plans

Tax Advantages

One of the most significant benefits of qualified plans is their tax advantages. Contributions to plans such as 401(k)s and Traditional IRAs are typically made with pre-tax dollars, reducing your taxable income in the year you contribute. This means you can defer taxes until you begin withdrawals in retirement, when you may be in a lower tax bracket. Additionally, the growth of investments within these accounts is tax-deferred, allowing your savings to compound without immediate taxation.

Employer Contributions

Many employers offer matching contributions to 401(k) plans, which can significantly enhance your total retirement savings. For instance, an employer might match a portion of your contributions, effectively giving you “free money” toward your retirement. This incentive can amplify your investment and is one reason to take full advantage of qualified plans at your workplace.

Portability

Many qualified plans offer portability, meaning that if you change jobs or retire, you can roll over your retirement savings into another qualified plan or an IRA without penalties. This flexibility allows you to maintain the tax advantages associated with your retirement funds while making it easier to manage your accounts as your career evolves.

Disadvantages of Qualified Retirement Plans

While qualified retirement plans offer numerous benefits, such as tax advantages and employer contributions, they also come with several disadvantages that participants should be aware of. Understanding these drawbacks can help individuals make informed decisions regarding their overall retirement strategy.

- One of the most significant drawbacks of qualified retirement plans is the contribution limits imposed by the Internal Revenue Service (IRS). For example, the 401(k) contribution limit for 2026 is $24,500 for employee salary deferrals and $70,000 for the combined employee and employer contributions. These limits may restrict higher earners from saving as much as they would like for retirement.

- The future tax rate on the income you withdraw from your plan is unknown. Taxes will be due on the principal and growth of your money when you take distributions from the plan. Most people expect tax rates to be higher in the future due to the out-of-control government spending and federal deficit. Therefore, you might get a small tax deduction as you contribute to your plan, but you are postponing taxes until later, when rates could be much higher.

- The distributions from your plan will also (negatively) affect the taxes on your Social Security benefits and the cost of Medicare.

- Qualified retirement plans are subject to strict rules regarding withdrawals. If participants take distributions before age 59½, they typically incur a 10% early withdrawal penalty in addition to income taxes on the amount withdrawn.

- Qualified retirement plans must comply with various complex regulations established by the IRS and ERISA.

- Many qualified retirement plans, such as 401(k)s, offer limited investment options, which may prevent participants from fully diversifying their portfolios.

- Qualified plans often incorporate vesting schedules for employer contributions. This means that employees may not fully own the employer’s contributions until they meet specific tenure requirements.

- Some qualified retirement plans may charge management fees, administrative costs, and other expenses that can erode investment returns over time.

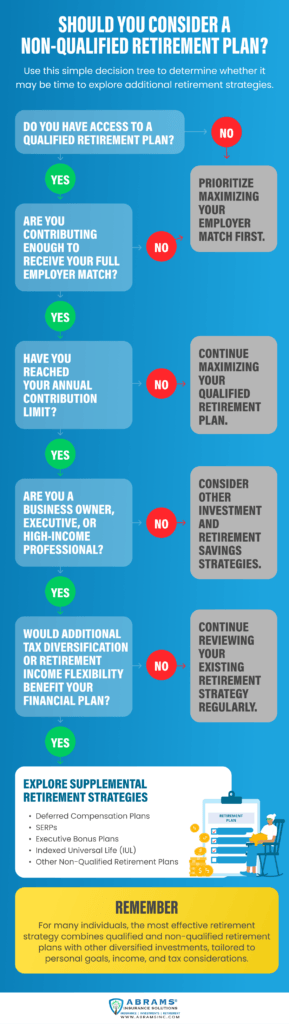

What Is a Non-Qualified Retirement Plan?

Nonqualified plans are retirement plans that do not meet the Internal Revenue Service (IRS) requirements to be considered “qualified.”

Unlike qualified plans, nonqualified retirement plans are not subject to the same rules and regulations, allowing for greater design and implementation flexibility. Nonqualified retirement plans offer employers an alternative for providing additional retirement benefits to select employees. They are often referred to as executive or supplemental retirement plans.

Types of Non-Qualified Plans

There are several types of non-qualified retirement plans, each designed to address specific retirement planning objectives.

Deferred Compensation Plans

A deferred compensation plan allows high-earning employees and executives to delay receiving a portion of their current income until a future date, typically retirement. By deferring compensation, participants may reduce their current taxable income while potentially receiving distributions during retirement when they may be in a lower tax bracket.

Supplemental Executive Retirement Plans (SERPs)

A Supplemental Executive Retirement Plan (SERP) is an extra retirement benefit that a company fully pays for to reward its top executives. Unlike a standard 401(k), the employee does not put any of their own money into it. The employer handles all the funding and decides the payout schedule. Companies mainly use SERPs to keep key leaders from leaving, as the money usually unlocks over time and is completely lost if the executive quits early.

Executive Bonus Plans

An Executive Bonus Plan is a straightforward strategy in which a company gives a selected employee a bonus to pay for a permanent life insurance policy. The employee owns the policy and may accumulate cash value over time while maintaining access to the death benefit. This arrangement can provide both retirement and legacy planning benefits while offering flexibility not available in traditional qualified retirement plans.

Split-Dollar Life Insurance Plans

Split-dollar life insurance is an arrangement in which the employer and employee share the costs and benefits of a life insurance policy. Depending on the structure, both parties may receive certain rights to the policy’s death benefit or cash value. These plans are commonly used for executive compensation and estate planning and can provide additional retirement-planning opportunities when structured appropriately.

Qualified vs Non-Qualified Retirement Plans Chart

| Feature | Qualified Retirement Plans | Non-Qualified Retirement Plans |

|---|---|---|

| IRS Approval | Required | Not Required |

| ERISA Rules | Generally Yes | Generally No |

| Examples | 401(k), 403(b), SEP IRA, SIMPLE IRA, Pension | Deferred Compensation Plans, SERPs, Executive Bonus Plans, IUL |

| Contribution Limits | IRS Limits Apply | Often More Flexible |

| Creditor Protection | Stronger | Varies |

| Tax Treatment | Tax Deferred or Roth | Depends on Design |

| Employee Eligibility | Must Meet Nondiscrimination Rules | Can Be Selective |

| Ideal Users | Most Workers | Executives and Business Owners |

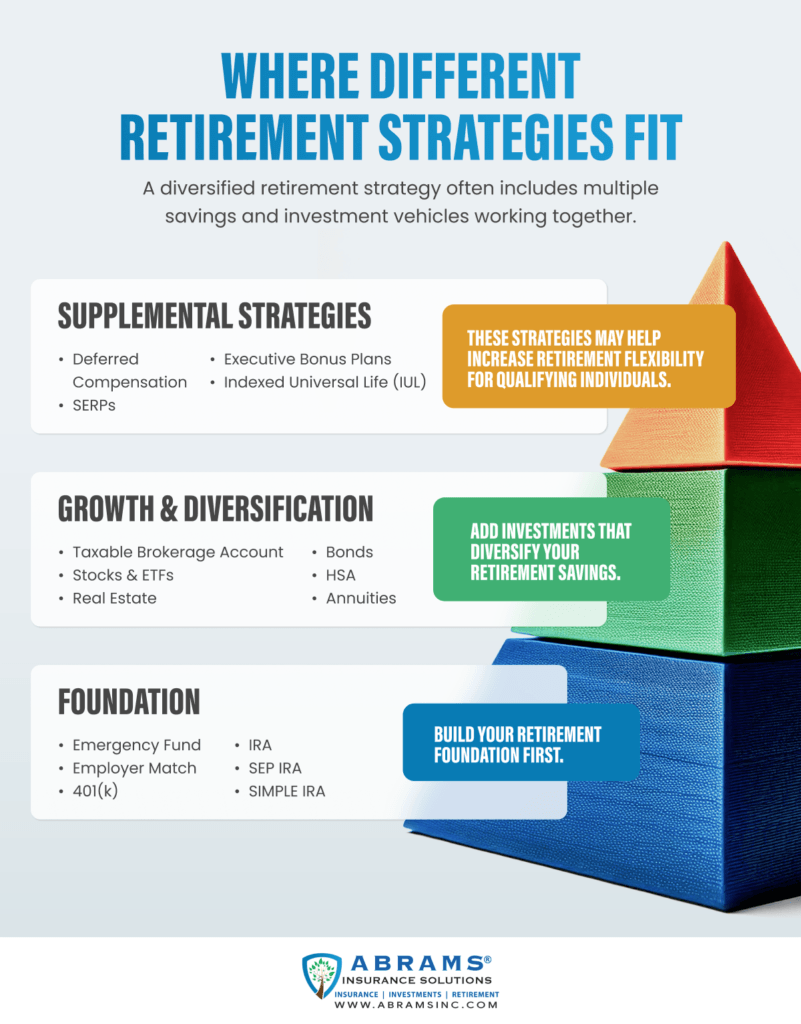

Popular Wealth Building Strategies

While qualified retirement plans and non-qualified retirement plans play an important role in retirement planning, they are only one part of the wealth-building landscape. Successful investors often diversify across multiple asset classes and income sources to help manage risk and create long-term financial security.

Some of the most common wealth-building strategies include:

- 401(k)s and 403(b)s

- IRAs, SEP IRAs, and SIMPLE IRAs

- Real estate investments

- Stocks, mutual funds, and exchange-traded funds (ETFs)

- Annuities

- Bonds and fixed-income investments

- Business ownership

- Passive income strategies, such as Airbnb rentals or book royalties.

- Cash value life insurance

Each strategy has its own advantages, risks, tax treatment, and liquidity characteristics.

One strategy that has gained increased attention among business owners, professionals, and high-income earners is Indexed Universal Life Insurance. While an IUL is not a qualified retirement plan and should not replace one, some individuals use it as a supplemental retirement income strategy because it offers life insurance protection, tax-advantaged cash value accumulation potential, and flexible access to policy values.

Let’s take a closer look at how Indexed Universal Life insurance works and where it may fit within a broader retirement strategy.

What is Indexed Universal Life Insurance?

Indexed Universal Life Insurance is a type of permanent life insurance that includes both a death benefit and a cash value component that can grow over time. It is not considered a qualified retirement plan like a 401(k) or IRA.

Some people use IULs as a supplemental retirement strategy because they offer tax-deferred growth and flexible access to cash value. The cash value is tied to the performance of a market index, such as the S&P 500, but you are not directly investing in the market. Instead, the insurance company credits interest based on index performance, within certain limits.

IUL policies also typically include downside protection, meaning your cash value won’t decrease due to market losses. However, this protection comes with limits on how much you can earn in strong market years.

Overall, an IUL can be used alongside traditional retirement accounts, but it is generally not a replacement for them. If you are deciding how to allocate your funds between the two, check out our breakdown of IUL vs 401(k) to see which fits your wealth strategy best.

A knowledgeable agent can establish the IUL with higher premium payments for a lower death benefit. Even though this might sound a bit strange, it actually helps you build cash value faster. The less you spend on the death benefit, the faster you build the cash value.

How Some People Use IUL as a Supplemental Retirement Strategy

One reason is tax diversification. Retirement income can come from taxable accounts, tax-deferred accounts, and tax-advantaged sources.

Some investors use IUL as an additional source of retirement assets that may provide greater flexibility when managing future taxes. Others appreciate the ability to access policy cash value without the early withdrawal penalties that may apply to certain qualified retirement plans. Moreover, IUL policies are not subject to required minimum distributions, giving policyholders more control over when they access policy values.

Some individuals also value the combination of retirement income potential and life insurance protection. If properly funded and managed, an IUL may provide access to cash value during retirement while also maintaining a death benefit for beneficiaries.

For most people, an IUL is best viewed as a complement to traditional retirement plans rather than a replacement for them.

Potential Advantages of IUL

- Provides permanent life insurance coverage along with cash value accumulation potential.

- Cash value grows on a tax-deferred basis.

- Policyholders may access cash value through withdrawals and policy loans.

- Most policies include downside protection that helps shield cash value from direct market losses.

- No IRS contribution limits like those imposed on many qualified retirement plans.

- No required minimum distributions (RMDs).

- Can provide a death benefit for beneficiaries.

- May help diversify retirement assets across different tax treatments.

Potential Drawbacks of IUL

- More complex than traditional retirement accounts such as 401(k)s and IRAs.

- Policy charges, insurance costs, and fees can impact performance.

- Growth may be limited by caps, participation rates, spreads, or other policy provisions.

- Requires long-term commitment to maximize potential benefits.

- Loans and withdrawals can reduce cash value and death benefits.

- Poor policy design or underfunding can negatively affect long-term results.

- Not appropriate for every investor or retirement objective.

- Generally works best as a supplement to qualified retirement plans rather than a replacement for them.

FAQs

What is the difference between a qualified retirement plan and a non-qualified retirement plan?

Qualified retirement plans, such as 401(k)s, 403(b)s, SEP IRAs, and pension plans, must comply with IRS and ERISA requirements. Non-qualified retirement plans generally offer more flexibility and are often used by business owners, executives, and highly compensated employees to supplement traditional retirement savings.

Is a 401(k) a qualified retirement plan?

Yes. A 401(k) is one of the most common types of qualified retirement plans. These employer-sponsored plans allow employees to make pre-tax or Roth contributions while benefiting from tax-advantaged growth. Many employers also offer matching contributions, making a 401(k) an important foundation for retirement savings.

Is a SEP IRA a qualified retirement plan?

Yes. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is considered a qualified retirement plan. SEP IRAs are commonly used by self-employed individuals and small business owners because they offer higher contribution limits than traditional IRAs and are relatively simple to administer.

What is a 403(b) Plan?

A 403(b) plan, similar to a 401(k), is a type of employer-sponsored plan specifically designed for employees of public schools, certain tax-exempt organizations, and some ministers. These employer-sponsored plans, named after the section of the Internal Revenue Code that governs them, allow employees to save for retirement on a tax-deferred basis, providing them the opportunity to accumulate savings without immediate tax liabilities.

What is an example of a non-qualified retirement plan?

Common examples of non-qualified retirement plans include deferred compensation plans, Supplemental Executive Retirement Plans (SERPs), executive bonus plans, and certain cash value life insurance strategies. These plans are often designed to provide additional retirement benefits beyond what is available through qualified retirement plans.

How do contributions to non-qualified plans differ from those to qualified plans?

Qualified retirement plans are subject to annual IRS contribution limits. For example, 401(k)s, SEP IRAs, SIMPLE IRAs, and other qualified plans have maximum contribution amounts that can change from year to year. Non-qualified retirement plans generally do not have the same IRS contribution limits, allowing some business owners, executives, and highly compensated employees to defer or contribute larger amounts toward retirement. However, contribution rules vary depending on the specific type of non-qualified plan and its structure.

Are non-qualified plans subject to ERISA?

Generally, non-qualified retirement plans are not subject to the same ERISA requirements as qualified retirement plans. As a result, they often offer greater flexibility but may not provide the same level of creditor protection or employee safeguards as ERISA-covered plans.

Can business owners use both qualified and non-qualified retirement plans?

Yes. Many business owners use a combination of qualified and non-qualified retirement plans. Qualified plans often serve as the foundation of a retirement strategy, while non-qualified plans may provide additional opportunities for tax diversification, supplemental income, and wealth accumulation.

Is IUL a qualified retirement plan?

No. IUL is not considered a qualified retirement plan under IRS rules. Instead, it is a form of permanent life insurance that some individuals use as a supplemental retirement strategy because of its potential for cash value accumulation, tax-deferred growth, and life insurance benefits.

Which retirement strategy is best for high-income earners?

There is no single retirement strategy that works for everyone. Many high-income earners begin with qualified retirement plans, then explore additional strategies once those contribution limits are reached. Depending on their goals, this may include taxable investment accounts, real estate, annuities, deferred compensation plans, or cash value life insurance. The most appropriate strategy depends on factors such as income, tax situation, risk tolerance, and retirement goals.

Qualified vs Non-Qualified Retirement Plans: Which Is Better?

Ultimately, choosing between a qualified and non-qualified plan doesn’t have to be an either-or decision.

Qualified retirement plans often provide valuable tax advantages and may include employer matching contributions, making them an excellent foundation for retirement savings. Non-qualified retirement plans can complement those savings by providing additional flexibility, higher contribution opportunities, and alternative tax treatment. Business owners, executives, and high-income professionals often use both qualified and non-qualified strategies as part of a diversified retirement plan.

At Abrams Insurance Solutions, we help you protect your hard-earned money, minimize your tax burden, and build a flexible income strategy for retirement, whether you are a business owner, an executive, or already retired.

Want to see the real math behind your retirement? Give us a call today at 858-703-6178 or request your personalized custom Wealth Report. We’ll put together a personalized IUL quote and show you a side-by-side breakdown of what happens when you put the exact same savings into a taxable, tax-deferred, or tax-advantaged account versus an IUL. It’s the clearest way to see how much more after-tax income you could have down the road.