Gifting Kai-Zen – A High Earner Case Study

Posted in Kai-Zen Life Insurance last updated on July 7, 2025

Posted in Kai-Zen Life Insurance last updated on July 7, 2025We work with a lot of folks who have set up one of these leveraged life insurance contracts, make their 5th and final premium payment, and then ask, “Now what?”

Usually, it’s a physician or a well-compensated executive.

They have a couple of options. They can have more than one plan. They’d set up a second one for themselves. The premium payments would start for another five years. Then they’ll realize they can do what many of their peers do, which is rinse and repeat.

But we’re also starting to get questions from these high earners about their kids.

Oftentimes the adult child just finished their degree at a university. Or they go into a less lucrative field than their parents and need help to afford one of these Kai-Zen plans on their own.

The biggest concerns we see from these parents when they want to help support their kids are:

- What if I need the money?

- What will my children do with it once I give it to them?

Usually, these parents have plenty of retirement income prepared. They don’t think they’ll need the extra money, but they want to be extra prepared, just in case.

Let’s look at a couple of case studies. We’ve changed the names for privacy reasons. But these cover:

- Wanting to make sure you have enough in retirement and providing for your children through the death benefit

- Worrying about your children not being able to afford retirement

This is part of the series on using life insurance for estate planning and leaving your adult children meaningful gifts for them to use later on. You can read the article on how this life insurance estate planning strategy works here.

What if I need the money for myself?

Stan is 54 and in great health. His kids are grown, and he feels like he’s prepared for retirement (still a ways off), but the current volatility of the market and the rising healthcare costs worry him.

He has a Kai-Zen for himself already. He just made his fifth and final payment.

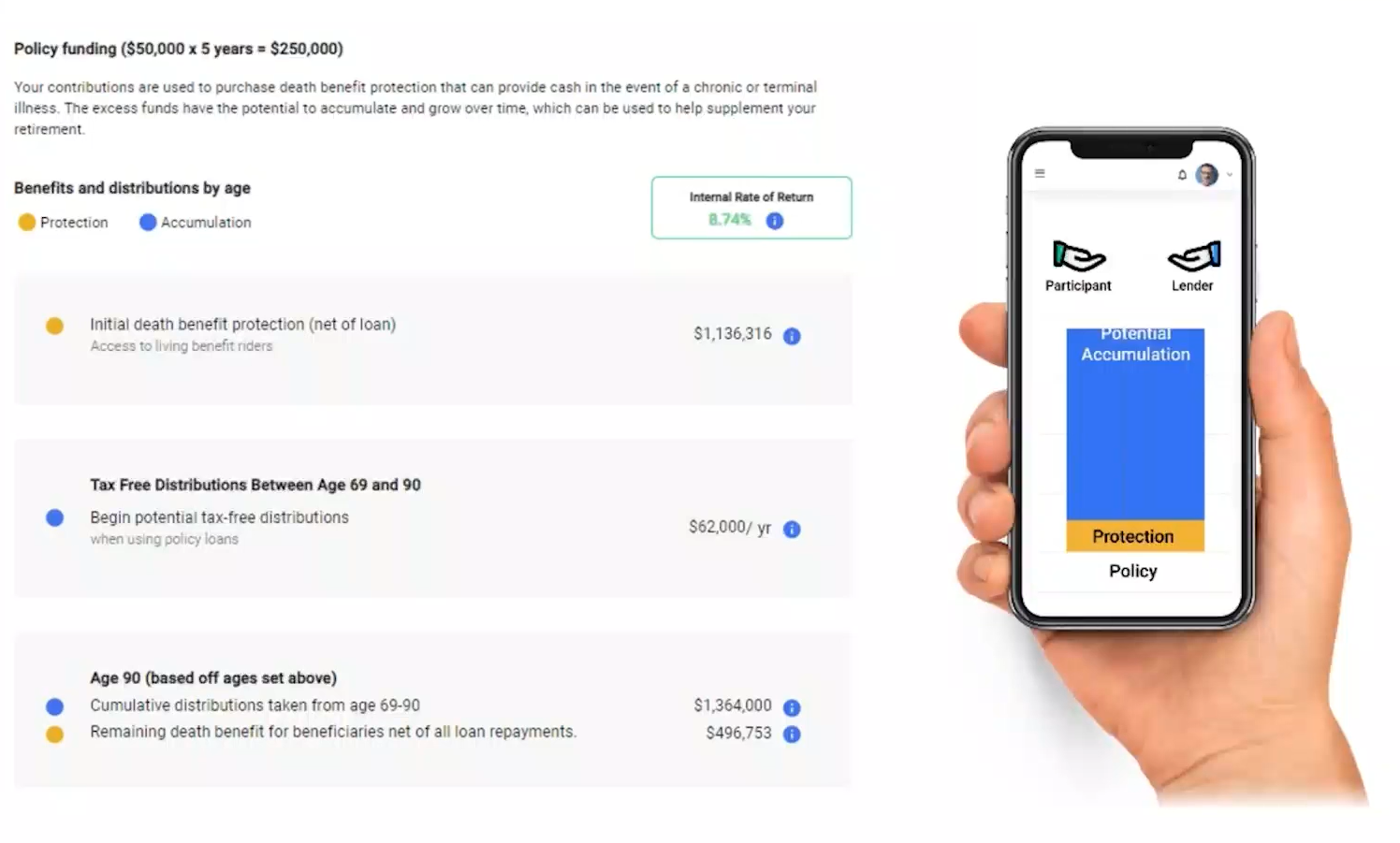

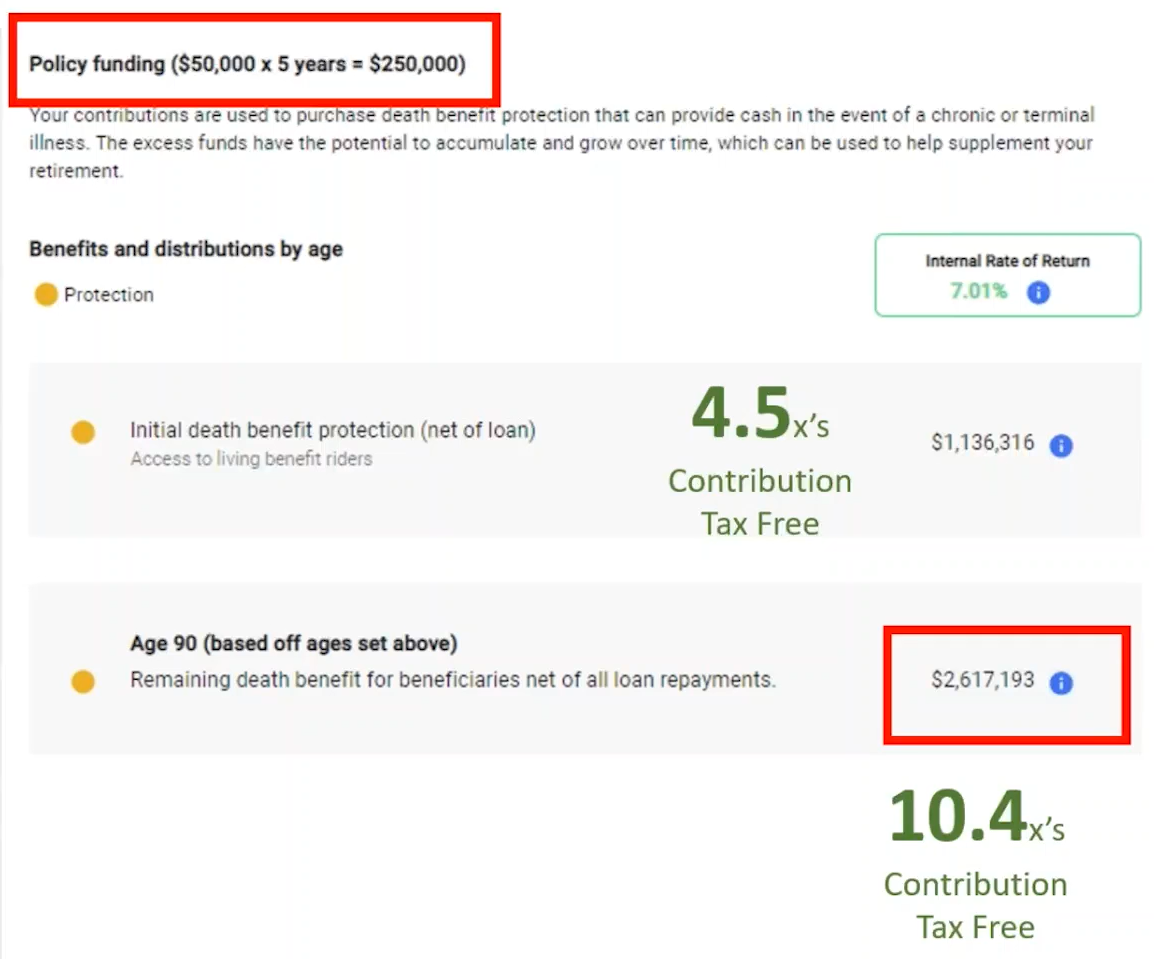

First, let’s look at how Stan could buffer his retirement income by getting a second Kai-Zen funding it at $50,000 a year for five years.

He’s looking at adding $62,000 a year of non-taxable income to his retirement from ages 69 to 90. That amounts to an extra $1,364,000.

Plus, he still has a nearly half million death benefit to pay estate taxes or go to his children. That’s nearly twice as much as Stan was considering gifting to his children in cash.

Stan could also use the living benefits on the policy to help out in the event of a long-term care event or chronic illness.

What if Stan wants to provide for his kids through the death benefit?

If he built a second leveraged life insurance policy with the same $50,000 contribution, he’d be leaving his kids over $2.5 million dollars at age 90. Or $1.1 million if he died the next day.

That’s 10.4x the quarter million he was considering giving to his kids. It’s also tax-free.

What About Leveraging a Gift For Adult Children?

Let’s look at a case study where a mom was worried about her children’s ability to save for retirement.

Anita and her husband wanted to provide for their two children in their late 20s. But they weren’t sure the timing was right to gift them cash.

What else could they do?

Anita already had a Kai-Zen on herself. She and her husband were maxing out their retirement contributions. With an annuity on top, they felt secure in their retirement planning.

The 2023 gift tax exclusion for couples is $34,000 per year.

Anita has two children. Dylan and Jessica. (Names changed for privacy reasons.)

Gifting to A Qualifying Child

Jessica is 30 and qualifies for Kai-Zen on her own. But with a new home and new baby, she does not want to make the financial commitment to getting her own Kai-Zen right now.

Since her income is in the six figures a year range, she qualifies for her own plan. The underwriters don’t care who pays for it as long as the insured person qualifies.

This one is easy.

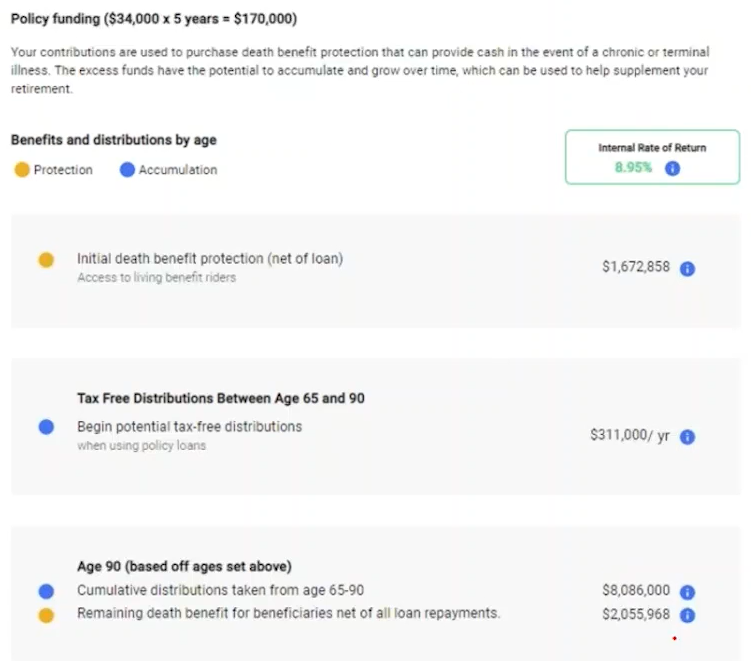

Jessica applies, and Anita pays for the five years of premiums at $34,000 each year, or $170,000 total.

This will grow for 15 years. Then Jessica can use that tax-free income for whatever she wants. Or maybe she’ll choose to hold onto it and use it for her own son’s college education. Or perhaps she’ll boost her retirement income.

Gifting to a Non-Qualifying Child

Dylan is 27. He earns $60,000 a year. That doesn’t qualify him for a Kai-Zen policy. Sure, he would qualify for a cash-value-focused indexed universal life policy, but you’ll see the difference in the image below about what kind of difference that leverage makes over many decades.

Anita also set up a Kai-Zen for Dylan. The underwriting process involved a letter of intent and proof that Anita had her own Kai-Zen plan. But that was the only difference between Dylan’s application process and Jessica’s.

Compound interest over decades is a beautiful thing. When Dylan retires, because of the five years of gifts from his parents, he’ll be making many times what he was during his working years, barring a change in career.

Starting at Dylan’s current age, 27, and letting that $170,000 grow until he’s 65, gives him a retirement income stream of $311,000 a year.

Dylan also can protect himself with the living benefits included with the policy in the event of a critical illness.

But Anita is thorough. Kai-Zen sounds great. She knows that. She already had a contract. But what would Dylan’s other options for investing that $170,000 look like?

If Dylan got the same type of life insurance policy without the leverage the bank provides through Kai-Zen, he’d see a distribution of $138,000 from age 65 to age 90. Still more than he’s making now, but the leverage just makes more sense.

If Dylan were the model of financial responsibility and took his parents’ gift and invested it in the market himself, he’d be looking at a retirement income stream of just over $60,000 a year. But then there are no life insurance living benefits in the event of a medical emergency.

And that’s assuming he invests every penny and doesn’t spend it on something else as his mother worried he might.

Who Qualifies for This Sort of Leverage Strategy?

First, if you’re younger than 55, here’s what you need to show the underwriter:

- Giftor must have at least $200,000 annual income (or $3+ million net worth)

- Giftor must provide 2 years of income verification

- Insured must also provide 2 years of income verification

- Cover letter if the insured does not financially qualify on their own

- Giftor must own a Kai-Zen policy for themselves

- If giftor is uninsurable, the above is waived but details must be included in the cover letter

You’re greater than 55, here is the other set of qualifications.

- Giftor must have at least $200,000 annual income (or $3+ million net worth)

- Giftor must provide 2 years of income verification

- Insured must also provide 2 years of income verification

- Cover letter if the insured does not financially qualify on their own

How Does a Kai-Zen Policy Work?

It’s all about leverage.

You contribute half of the premiums for five years. The bank contributes half for five years and then 100% for the next five.

After 15 years of growth, tied to (not invested in) a market index, your cash value has grown enough that the bank can take back its investment, and you still have the cash value with its hyper-boosted growth to draw from whenever you wish.

For an in-depth look at how it’s funded, grows, and avoids taxes, read this article on building wealth with life insurance plus leverage.

Next Steps

Every case is a little different. If you want to see some “what if” scenarios for your family, give us a call at (888) 905-0333. And if you’re under 55 years of age, you’ll need your own policy before the insurance company will issue any for your children.

Curious to see how much Kai-Zen can benefit you or your children? Click here to estimate your benefits.

2 Comments

Holly

I like to know more about kaizenafter 15 year then how much I got yearly ans how lomg I got yearly money If I am 50 now and I will pay $2000 per month for 5 year ?

Thanks

Holly

Chris Abrams

Hi Holly: Please see the following page for benefit estimates: https://kaizen.simplicityniw.com/dd91c858-1e37-44bc-9b40-d6fe4c2a8dee. Click "Learn About Kai-Zen" on this page and go to "2. Estimate Your Benefits". This will show you a comparison of future income between a Kai-Zen plan and other options. Let me know if you have any additional questions.