IUL vs 401(k): What to Choose for Retirement?

Posted in Indexed Universal Life (IUL) last updated on July 9, 2026

Posted in Indexed Universal Life (IUL) last updated on July 9, 2026If you are comparing an IUL vs. a 401(k) to determine which is better for retirement, it’s rarely about choosing one over the other. A 401(k) is often the best starting point, especially with employer matching. Whereas, a properly designed max-funded IUL can complement a 401(k) by providing additional tax benefits, cash value growth, downside market protection, and flexible access to money during retirement.

Estimated reading time: 18 minutes

Key Takeaways

- A 401(k) and an Indexed Universal Life (IUL) policy serve different purposes and shouldn’t be viewed as direct replacements for one another.

- For many employees, contributing enough to receive the full employer match should be a top priority.

- A properly structured, max-funded IUL can complement a 401(k) by providing tax diversification, downside protection, and flexible access to cash value.

- Investment returns are only one part of retirement planning. Taxes, market risk, income flexibility, and legacy planning are equally important considerations.

- There is no single retirement account that provides every benefit. Many successful retirement plans combine multiple strategies.

- The best retirement strategy depends on your financial goals, tax situation, and risk tolerance.

IUL vs 401(k) is one of the most debated topics in retirement planning, and for good reason. Most people rely on a 401(k), but it doesn’t offer everything you need. While a 401(k) helps you save, cash-value life insurance adds an extra layer of protection to your savings. By combining the two, you can enjoy the growth of your investments

Throughout this guide, we’ll compare an IUL and a 401(k) on key factors, including taxes, investment growth, market risk, retirement income, flexibility, liquidity, and estate planning.

Table of Contents

- Key Takeaways

- The Retirement Question Most People Ask (and Why It’s the Wrong One)

- What is a 401(k)?

- What is Indexed Universal Life Insurance (IUL)?

- IUL vs 401(k): Key Differences

- IUL vs 401(k): Which Retirement Strategy Is Right for You?

- There Is No Perfect Retirement Account

- Comparing Retirement Income Strategies

- FAQs

- Questions to Ask When Weighing IUL vs 401(k)

- Request Your Complimentary Retirement & Wealth Report

The Retirement Question Most People Ask (and Why It’s the Wrong One)

Most people searching for “401(k) vs IUL” are really trying to answer one question: “Where should I put my next retirement dollar?” That’s a fair question, but it can lead you down the wrong path if you treat these two options as direct substitutes. Comparing an IUL to a 401(k) is a bit like comparing homeownership to investing in the stock market—each serves a different purpose, and the better choice depends on your financial goals.

Before we compare the two side by side, let’s first look at how each strategy works.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement savings plan that allows you to invest for retirement while receiving valuable tax benefits. You make contributions through automatic payroll deductions, which helps you build a consistent and disciplined approach to long-term saving.

While a 401(k) is one of the most effective retirement savings tools available, it’s important to understand what it was designed to do and where it may have limitations. That context will make it much easier to compare it with an Indexed Universal Life policy later in this guide.

How a 401(k) Works

One of the biggest reasons 401(k) plans have become so popular is their simplicity.

When you enroll, you choose how much of each paycheck you want to contribute. Your employer automatically deducts those funds and deposits them into your retirement account before you get paid. You then invest that money into the plan’s available options, such as mutual funds, index funds, or target-date funds.

Here’s one example:

Suppose you earn $80,000 per year and choose to contribute 10% of your salary. This means you direct $8,000 into your 401(k) over the course of the year. If your employer offers a 4% match, they contribute an additional $3,200, bringing your total annual retirement savings to $11,200.

When you contribute to a traditional 401(k), your $8,000 contribution reduces your taxable income for the year. You then invest your money in options such as mutual funds or index funds, allowing your money to grow tax-deferred until you withdraw it in retirement.

Over time, this combination of consistent contributions, employer matching, and market-based growth can help build a substantial retirement balance.

Why Millions of Americans Choose a 401(k)

For many employees, a 401(k) is one of the easiest ways to build long-term wealth.

Automatic payroll deductions make saving consistent, employer matching adds extra contributions, and traditional plans may reduce your taxable income while allowing investments to grow tax-deferred. These benefits make 401(k)s a popular retirement tool, but they still carry limits. Investments are subject to market risk, withdrawals are typically taxable, and options are restricted to your employer’s plan.

Because of these limitations, many people eventually look for additional strategies to complement their 401(k) plans.

Is a 401(k) Right for You?

For most professionals, a 401(k) is the smartest place to start saving for retirement. However, as your income grows, your retirement goals may evolve as well. You begin thinking about reducing taxes, creating flexible income, protecting your family, or leaving a legacy to future generations. These are some of the reasons people begin exploring strategies beyond a traditional 401(k), including Indexed Universal Life insurance.

Before comparing the two side by side, let’s look at how an IUL works and why some people use it as part of their retirement plan.

What is Indexed Universal Life Insurance (IUL)?

An Indexed Universal Life (IUL) policy is a type of permanent life insurance that provides both a death benefit and a cash value component that can grow over time. While its primary purpose is to provide financial protection for your beneficiaries, many people also use an IUL as part of a long-term retirement strategy because of its unique tax advantages and flexibility.

Unlike a 401(k), an IUL isn’t an employer-sponsored retirement plan or an investment account. Instead, it’s a life insurance policy that can accumulate cash value based on the performance of a stock market index, without investing directly in the stock market.

How an IUL Works

An Indexed Universal Life policy works differently from a traditional retirement account. Each premium you pay is divided into different purposes. A portion covers the cost of the life insurance and policy expenses, while the remainder is credited to the policy’s cash value.

Rather than purchasing stocks or mutual funds (like in a 401(k) plan), the cash value earns interest based on the performance of a stock market index, such as the S&P 500. If the index increases, your policy may receive interest up to the limits established by the policy, such as participation rates or caps. If the index performs poorly or declines, your cash value is generally protected from market losses by a contractual floor, provided the policy remains in force and subject to the terms of the contract.

Over time, the cash value can grow on a tax-deferred basis. Later in life, many policyholders access a portion of that accumulated cash value through policy loans, which may provide tax-free retirement income when the policy is properly structured and managed.

How People Use an IUL for Retirement

Once they’ve accumulated sufficient cash value, many policyholders begin using a portion of it to supplement income from other retirement sources, such as a 401(k), IRA, pension, or Social Security. Rather than replacing these income sources, an IUL is often used to provide additional flexibility and tax diversification throughout retirement.

Many policyholders work with a financial professional to determine an annual borrowing limit for their policy. This strategy creates a stream of supplemental retirement income while keeping the policy active throughout retirement.

This approach eliminates Required Minimum Distributions (RMDs). Unlike many qualified retirement accounts, an IUL doesn’t force you to take withdrawals at a certain age. Instead, you decide when, how much, and whether to access your policy’s cash value based on your personal income needs and tax situation.

Another unique feature is that policy loans generally don’t reduce the amount of cash value that continues to earn indexed interest. In many policies, interest is credited on the full cash value while the loan remains outstanding, although loan interest and policy terms still apply. Over time, this can help sustain the retirement income strategy in the long term when the policy is properly designed and managed.

Lastly, if there is a remaining death benefit when you pass away, it gets paid to your beneficiaries tax-free. That means an IUL can help support both your retirement income goals and your legacy planning objectives.

Of course, there are some important considerations. The policy must be appropriately designed, consistently funded, and managed throughout retirement. Taking excessive loans or allowing the policy to lapse could create unintended tax consequences, which is why it’s important to review your strategy regularly with an experienced financial professional.

IUL Caps, Participation Rates, and Internal Fees

To evaluate an IUL accurately, you have to understand its internal moving parts. Unlike a 401(k), where costs are tied to fund expense ratios, an IUL has front-loaded insurance costs and administration fees (which often run higher in the early years of the policy).

Additionally, insurance carriers establish index caps (ceilings on your maximum annual growth) and participation rates. Because carriers can adjust these variables over time, working with a strategist to review your policy regularly and ensuring it is continuously max-funded is essential to keeping your retirement timeline on track.

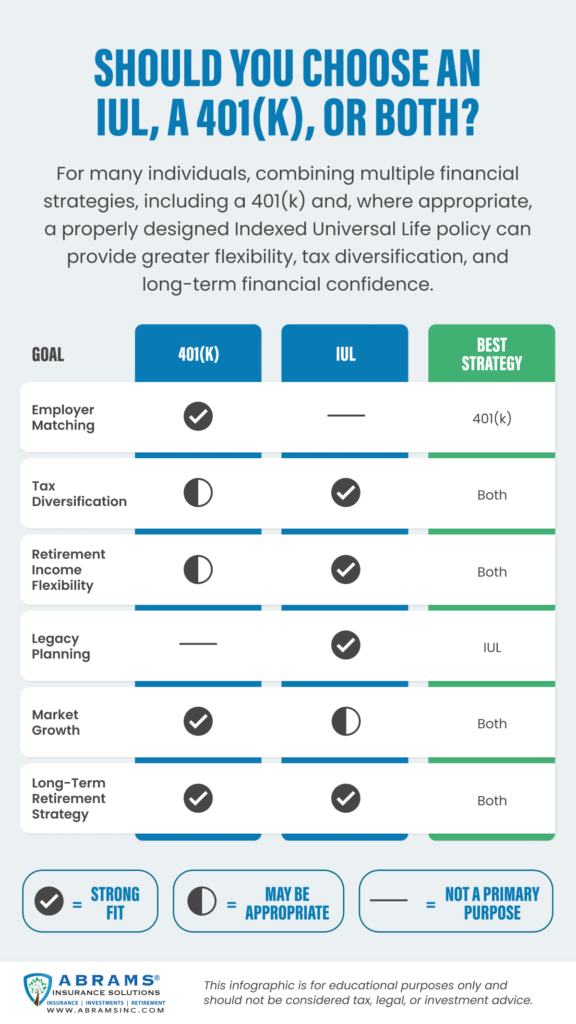

IUL vs 401(k): Key Differences

Now that you understand how each strategy works on its own, it’s easier to compare them side by side.

While both can play an important role in retirement planning, they were designed for different purposes. A 401(k) helps you accumulate retirement savings through workplace investing. At the same time, an Indexed Universal Life policy combines permanent life insurance with the opportunity to build tax-advantaged cash value over time.

The table below highlights some of the biggest differences between the two:

| Features | 401(k) | IUL |

|---|---|---|

| Primary Purpose | Retirement savings | Life insurance with cash value accumulation |

| Contributions | Payroll deductions | Flexible premium payments |

| Tax Treatment | Tax-deferred | Tax-deferred growth; potential tax-free access through policy loans* |

| Employer Match | Often available | Not available |

| Market Exposure | Directly invested | Not directly invested |

| Downside Protection | No | Yes, subject to policy terms |

| Retirement Income | Generally taxable | Policy loans may be tax-free* |

| Required Minimum Distributions | Yes (Traditional 401(k)) | No |

| Death Benefit | No | Yes |

| Access Before Retirement | Limited; penalties may apply | Flexible access through policy loans and withdrawals, subject to policy terms |

*Policy loans are generally tax-free as long as the life insurance policy remains active (in force). If a policy lapses or is surrendered with an outstanding loan, the borrowed amount above what you paid into the policy (your basis) could become taxable.

How Taxes Differ Between an IUL and a 401(k)

A 401(k) offers upfront tax savings, but withdrawals are taxed later, while an IUL uses after-tax contributions and may provide tax-advantaged income through policy loans. Another key difference is flexibility: 401(k)s require minimum distributions, but IULs do not.

“Investment diversification is important, but tax diversification can be just as valuable. In retirement, it’s not just what you’ve saved that matters. It’s how much you’re able to keep after taxes.” – Chris

After more than 17 years of helping people prepare for retirement, one of the biggest mistakes I see is failing to diversify tax risk. Many people diligently save every retirement dollar in a traditional 401(k) or IRA without realizing they have a silent partner in those accounts: the IRS.

For example, if you accumulate $1 million in a traditional 401(k) and your effective tax rate in retirement is 35%, roughly $350,000 could ultimately go toward taxes, leaving about $650,000 to support your retirement lifestyle. Actual tax rates will vary based on your circumstances, but the example illustrates how taxes can significantly affect your spendable retirement income.

Of course, none of us knows what tax rates will be 10, 20, or 30 years from now. However, with the national debt continuing to grow and the federal government running large annual deficits, many economists and financial professionals believe higher taxes remain a real possibility over the long term. The Congressional Budget Office projects that federal debt held by the public will climb from about 101% of GDP in 2026 to 120% by 2036 under current law. That’s why I encourage clients to build tax diversification, not just investment diversification.

Depending on your situation, that may include a combination of traditional retirement accounts, Roth IRAs or Roth 401(k)s, and properly structured cash value life insurance. Having money in different tax “buckets” gives you greater flexibility and may help reduce the impact of future tax changes during retirement.

How Investment Risk Differs Between an IUL and a 401(k)

A 401(k) exposes you directly to market growth, but it also exposes you to market losses. An IUL takes a different approach—the insurance company does not invest your cash value directly in the market, which protects your principal from downturns while still crediting your account with indexed interest up to the policy limits. For many people, the decision comes down to how much market risk they want to take and whether they want to add a more conservative asset to their portfolio.

Max Funded IUL vs 401(k): What’s the Difference?

A 401(k) is an employer-sponsored retirement plan with IRS contribution limits, while a max-funded IUL is a permanent life insurance policy intentionally structured to maximize cash value growth while maintaining its tax benefits. Many high-income earners use max-funded IULs to complement their traditional retirement plans.

IUL vs 401(k): Which Retirement Strategy Is Right for You?

By now, you’ve probably realized there isn’t a universal winner in the IUL vs 401(k) debate. The right strategy depends on your income, age, tax bracket, retirement goals, and overall financial situation.

A 401(k) May Be the Better Choice If…

You’re early in your career, or your employer offers matching contributions. It can also make sense if your primary goal is lowering your taxable income today and you’re comfortable with long-term market investing.

An IUL May Be Worth Considering If…

You’ve already established retirement savings and are looking for additional tax diversification, greater flexibility in retirement, or permanent life insurance protection. It can also appeal to individuals who are concerned about future tax rates or want to reduce their exposure to market downturns.

Use a Max-Funded IUL to Complement Your 401(k)

For many successful professionals, business owners, and higher-income families, the answer isn’t choosing one strategy over the other. Instead, they use a 401(k) to capture employer-matching contributions and build long-term retirement assets, while adding a max-funded IUL to create another source of tax-advantaged retirement income and greater financial flexibility.

Ultimately, the best retirement strategy isn’t determined by the features of a particular financial product. It’s determined by how well your overall plan supports your long-term financial goals. That’s why two people with the same income can arrive at completely different recommendations based on their ages, family situations, tax outlooks, and retirement objectives.

The good news is you don’t have to figure it out on your own.

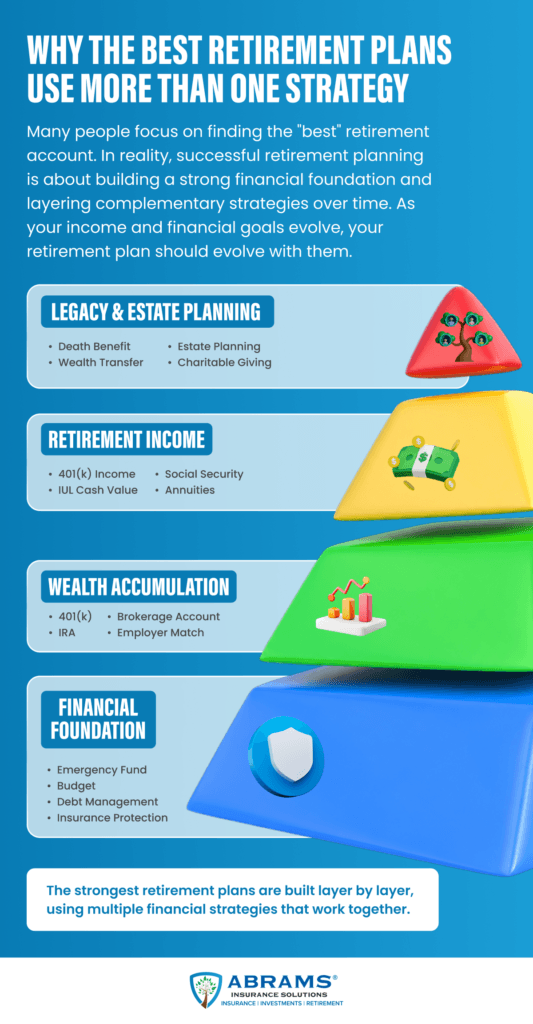

There Is No Perfect Retirement Account

One of the biggest mistakes in retirement planning is searching for a single account that does everything. In reality, no retirement strategy offers growth, tax advantages, downside protection, flexibility, income, and legacy benefits all in one. Each option, whether it’s an IUL or a 401(k), is designed to solve different financial needs and comes with its own trade-offs.

Let’s look at the comparison chart below, which shows how various retirement strategies stack up across the features people value most.

Retirement Strategy Feature Checklist

| Feature / Benefit | 401(k) / IRA (Tax-Deferred) | Roth IRA (Tax-Free) | Taxable Brokerage Account | Indexed Universal Life (IUL) |

|---|---|---|---|---|

| Tax-Deferred Growth | ✅ | ✅ | ❌ | ✅ |

| Tax-Free Withdrawals | ❌ | ✅ | ❌ | ✅ (if structured properly) |

| Upfront Tax Deduction | ✅ | ❌ | ❌ | ❌ |

| No Contribution Limits | ❌ | ❌ | ✅ | ✅ |

| No Income Restrictions | ✅ | ❌ | ✅ | ✅ |

| Market Loss Protection | ❌ | ❌ | ❌ | ✅ (floor protection) |

| Participation in Market Gains | ✅ | ✅ | ✅ | ✅ (with caps/limits) |

| Required Minimum Distributions (RMDs) | ✅ | ❌ | ❌ | ❌ |

| Flexible Access to Funds | ⚠️ (penalties may apply) | ⚠️ (rules apply) | ✅ | ✅ (via policy loans) |

| Tax Diversification | ❌ | ✅ | ✅ | ✅ |

| Retirement Income Flexibility | ⚠️ | ✅ | ✅ | ✅ |

| Death Benefit / Legacy Planning | ❌ | ❌ | ❌ | ✅ |

| Protection from Sequence Risk | ❌ | ❌ | ❌ | ✅ |

Key Takeaway:

Each strategy offers unique advantages, but none provides all the benefits. A well-rounded retirement plan often combines multiple account types to balance growth, tax efficiency, flexibility, and protection.

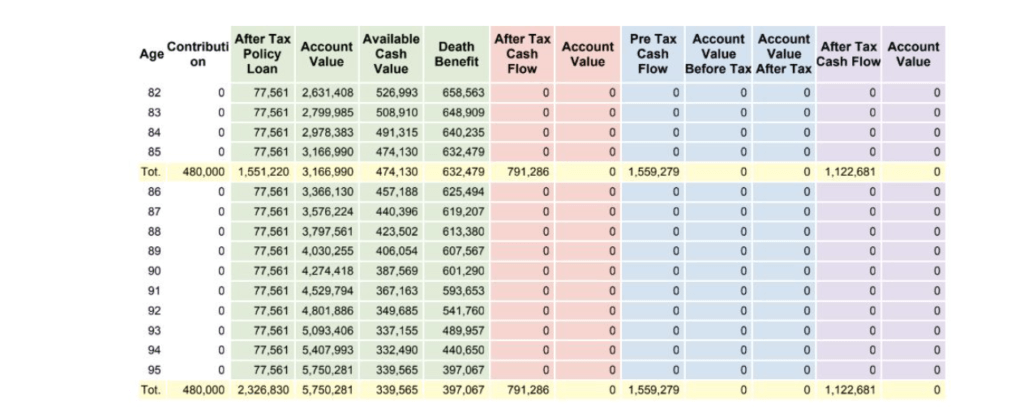

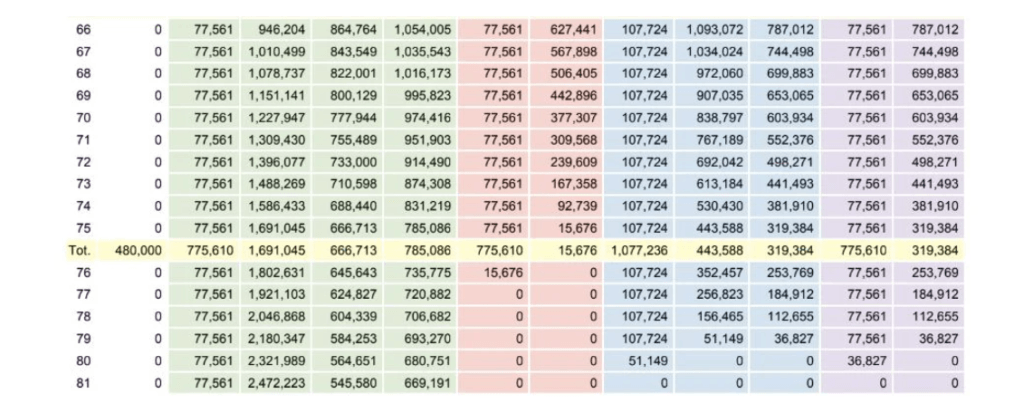

Comparing Retirement Income Strategies

Features are important, but what ultimately matters is how your retirement strategy supports you after you stop working.

The following examples illustrate how different types of retirement accounts may perform over time, depending on their tax treatment and withdrawal strategies. While every person’s situation is different, these examples demonstrate why taxes, market performance, and withdrawal planning can significantly affect how long your retirement savings last.

As retirement begins, the differences become even more apparent. Taxable accounts, tax-deferred accounts, tax-free strategies, and properly structured IUL policies each produce different levels of after-tax income and may last for different periods depending on market performance, tax rates, and withdrawal patterns.

These charts show how running out of money in retirement may unfold. When we analyze longevity in retirement with consistent income withdrawals, the taxable account depletes by age 76, while the tax-deferred and tax-free accounts last until age 80. In contrast, the IUL continues to provide financial support through age 95 and beyond. Plus, the IUL also offers a sizable death benefit for your loved ones.

The best strategy is to maximize your participation in qualified retirement plans, especially to fully capitalize on any employer-matching contributions. After securing these advantages, it’s wise to consult a financial advisor to explore additional tax-free options, such as Indexed Universal Life Insurance (IUL), to develop a well-rounded, effective retirement strategy.

Read Next: A Guide to Qualified vs. Non-Qualified Retirement Plans

FAQs

Should I invest in a 401(k) or an IUL?

For many people, it’s not either-or. Start with a 401(k), especially if there’s an employer match. Then consider a properly designed IUL to add tax diversification, flexible access to cash value, and permanent life insurance. The best approach depends on your goals and tax situation.

Can I contribute to both a 401(k) and an IUL?

Yes. An IUL is not a qualified retirement plan, so contributing to one doesn’t prevent you from contributing to a 401(k). Many higher-income professionals and business owners use both strategies as part of a diversified retirement plan.

What is a max-funded IUL?

A max-funded IUL policy maximizes your cash value growth while keeping the policy within IRS guidelines for life insurance. Unlike traditional life insurance policies that primarily provide a death benefit, you structure a max-funded IUL to build supplemental retirement income and long-term tax diversification.

Can I lose money in an IUL?

A properly designed IUL generally protects your cash value from market losses due to index performance, subject to the policy’s terms and provided the policy remains in force. However, policy charges, loans, withdrawals, or poor policy performance over time can affect cash value, so it’s important to understand how the policy works before purchasing one.

What happens if I stop paying premiums on an IUL?

Your policy’s structure and its accumulated cash value determine your options. In some cases, you can use existing cash value to keep the policy in force for a period of time. If you let the policy lapse, however, you could lose your coverage and face tax consequences on any outstanding policy loans. Your financial professional can help you understand the options available for your specific policy.

Is an IUL better than a Roth IRA?

An IUL and a Roth IRA serve different purposes. A Roth IRA is a retirement account that offers tax-free qualified withdrawals, while an IUL provides permanent life insurance along with the potential to build tax-advantaged cash value. Depending on your income, retirement goals, and eligibility, one or both may have a place in your overall financial plan.

Do wealthy people use IULs?

Some do. High-income earners and wealthy families may use properly designed IULs for tax diversification, supplemental income through policy loans, estate planning, and a tax-free death benefit. It’s typically one part of a broader financial plan.

Do business owners use life insurance policies, such as an IUL or a whole life policy?

Yes. Many business owners use permanent life insurance as part of their overall financial and business planning strategy. Depending on their objectives, a policy may help provide key person protection, fund buy-sell agreements, support executive benefit plans, build supplemental retirement assets, or create a tax-efficient legacy.

Questions to Ask When Weighing IUL vs 401(k)

Before deciding which retirement strategy may be right for you, it helps to look closely at how the features of an IUL vs 401(k) align with your personal situation.

- Am I contributing enough to my 401(k) to receive my full employer match?

- What tax bracket do I expect to be in during retirement?

- How important is it to protect part of my retirement savings from market downturns?

- Do I need permanent life insurance as part of my overall financial plan?

- Would additional tax diversification improve my retirement income strategy?

- What are my long-term financial goals for retirement and my family?

If you’re unsure how to answer one or more of these questions, a personalized retirement analysis can help you evaluate your options and determine which strategies best align with your goals.

At Abrams Insurance Solutions, we rarely recommend replacing one strategy with another. Instead, we help clients build retirement plans that combine multiple financial tools based on their goals, tax situation, and timeline.

Request Your Complimentary Retirement & Wealth Report

Our complimentary Retirement & Wealth Report is designed to help you evaluate your current retirement strategy and identify opportunities to improve it. We’ll review where you are today, discuss your retirement goals, and show you how a 401(k), a max-funded IUL, or a combination of both may fit into your long-term financial plan.

Whether you’re just beginning to save for retirement or looking to make your existing plan more tax-efficient, you’ll receive personalized recommendations based on your unique circumstances.

Schedule your complimentary Retirement & Wealth Report today and discover how the right retirement strategy can help you build wealth more efficiently, reduce unnecessary taxes, and retire with greater confidence.