Life Insurance for Drug Addicts with Opiate Addiction

Posted in Health Conditions last updated on February 10, 2026

Posted in Health Conditions last updated on February 10, 2026Finding life insurance for drug addicts, including those with a history of opioid or opiate addiction, can feel overwhelming. Many people assume they are automatically disqualified or that coverage is impossibly expensive. That’s not true.

Life insurance is still possible in many cases. The key is understanding how insurers evaluate risk, how addiction history is viewed differently from prescription use, and which options exist at each stage of recovery.

This guide explains everything you need to know about life insurance with opiate addiction, including recovery timelines, underwriting rules, overdose considerations, and when alternatives like accidental death insurance may apply.

Quick Summary

In short, people with a history of opioid or drug addiction can still qualify for life insurance, especially after documented recovery. Coverage options range from guaranteed-issue policies during early recovery to fully underwritten term or whole-life insurance after several years of sobriety. Understanding underwriting rules, overdose exclusions, and recovery timelines is key to protecting your family.

Why Life Insurance Still Matters After Opiate Addiction

Life insurance is not about waiting for the worst-case scenario; rather, it is meant to safeguard the financial security of those who rely on you. For families affected by opioid addiction, the financial risks are often higher. These risks may include mounting medical debt, potential income loss, outstanding loans or mortgages, and final expenses.

Securing coverage helps ensure that if something unexpected happens, your family is not left scrambling financially.

Another important thing to remember is that life insurance companies do not make moral judgments. They assess risk based on medical history, recovery stability, and overall health.

How Life Insurance Companies Define Opiates

From an underwriting perspective, opiates (opioids) are treated as a single drug category. This includes both legal prescription medications and illegal substances.

Common Prescription Opiates Reviewed by Insurers

- Oxycodone (OxyContin, Percocet)

- Hydrocodone (Vicodin, Norco)

- Morphine

- Fentanyl

- Methadone

- Codeine

- Hydromorphone (Dilaudid)

The recreational street varieties (heroin and opium) are also medically opiates, but are illegal to prescribe.

When applying for coverage, companies typically look at the following factors:

- The Substance Type: Opiates (including prescription painkillers, fentanyl, and heroin) are viewed with higher scrutiny than substances like marijuana or even alcohol due to the higher risk of a life insurance claim for drug overdose.

- The Recovery Timeline: This is the most critical factor. Most “traditional” carriers want to see at least 2 to 5 years of documented sobriety before offering standard rates.

- Medical Complications: Underwriters look for secondary health issues such as Hepatitis C, HIV, or liver damage, which often correlate with long-term drug use.

- Lifestyle Stability: Steady employment and stable housing are “green flags” that suggest a lower risk of relapse.

Prescription Opiate Use vs Opiate Addiction

This distinction is critical. Many Americans have used prescription opioids for legitimate medical reasons such as surgery, injuries, or chronic pain management. However, any opioid use triggers deeper underwriting review, even when no addiction exists.

Why Insurers Investigate Prescription Use

When evaluating life insurance applications, underwriters often see opiate prescriptions as indicators of underlying health conditions or potential risks. These prescriptions can signify a serious injury or illness, ongoing pain management needs, or a possible risk of dependency.

Insurance companies assess the severity of opioid use on a spectrum. On the less concerning end, a temporary prescription used for short-term pain is less risky. This may result from an injury that has no lasting effects. However, the stakes increase with injuries that cause residual pain or require long-term management for chronic pain conditions. The most concerning scenario is when there is evidence of dependency or misuse.

Transparency is crucial for applicants, so it’s essential to disclose any opioid prescriptions when applying for life insurance. Insurers will verify this information by cross-referencing national prescription databases.

Types of Life Insurance for Drug Addicts and Those in Recovery

Quick Answer:

The type of life insurance available depends largely on sobriety duration, with guaranteed issue options during early recovery and fully underwritten policies becoming available after several years of documented stability.

Depending on where you (or your loved one) are in the journey, different products will be more or less accessible.

Fully Underwritten Term or Whole Life

This is the “gold standard.” It requires a medical exam and a deep dive into your medical records.

- Best for: Individuals with 5+ years of documented sobriety.

- The Advantage: You get the lowest possible rates and the highest coverage amounts.

Apply for Whole Life Insurance

Simplified Issue Life Insurance

This requires no medical exam, but you must answer a series of health questions.

- Best for: Those with 2–3 years of recovery who may have minor lingering health issues.

- The Caveat: If you answer “Yes” to questions about recent drug treatment, you may still be declined.

Apply for Simplified Issue Life Insurance

Guaranteed Issue (GI) Life Insurance

As the name suggests, you cannot be turned down. There are no medical questions and no exams.

- Best for: Those currently struggling with addiction or in very early recovery (under 1 year).

- The Limitation: Coverage amounts are usually capped (often at $25,000), and there is typically a “graded death benefit,” meaning if you die within the first two years of the policy, your beneficiaries may only receive a refund of premiums plus interest.

Apply for Guaranteed Issue Life Insurance

Group Life Insurance

Many employers offer life insurance as a benefit. These policies are often “guaranteed issue” up to a certain amount (e.g., $50,000 or 1x your salary).

Expert Tip: This is often the easiest and cheapest way for someone with a history of addiction to get immediate coverage without a background check.

The Sobriety Milestone Table

Rates and eligibility are estimates and vary significantly by carrier, age, and overall health.

| Years in Recovery | Likely Coverage Option | Premium Expectation |

| Active Use | Guaranteed Issue Only | High (per $1k of coverage) |

| < 1 Year | Guaranteed Issue / Group Life | High |

| 1–3 Years | Simplified Issue / High-Risk Term | Moderate to High |

| 3–5 Years | Standard Term / Whole Life | Standard (with a “flat extra”) |

| 5+ Years | Standard to Preferred Term | Standard / Market Rates |

These timelines reflect common underwriting patterns, not guarantees. Individual outcomes vary by insurer, health profile, and recovery history.

Medication-Assisted Treatment (MAT) and Life Insurance

Medication-Assisted Treatment (MAT) is a medically supervised approach used to help individuals recover from opioid or alcohol dependence by combining FDA-approved medications with ongoing medical care and behavioral support.

Common MAT medications include Suboxone, methadone, and naltrexone, which work by reducing cravings, preventing withdrawal symptoms, and stabilizing brain chemistry so individuals can function normally and focus on long-term recovery.

From a life insurance underwriting standpoint, participation in a MAT program does not automatically disqualify an applicant. Insurers are typically more concerned with whether the treatment is physician-supervised, whether the dosage is consistent, whether there have been no recent relapses, and whether the individual demonstrates overall stability in health, employment, and daily life.

Because underwriting guidelines vary widely, some life insurance carriers are significantly more MAT-friendly than others, making carrier selection and experience especially important.

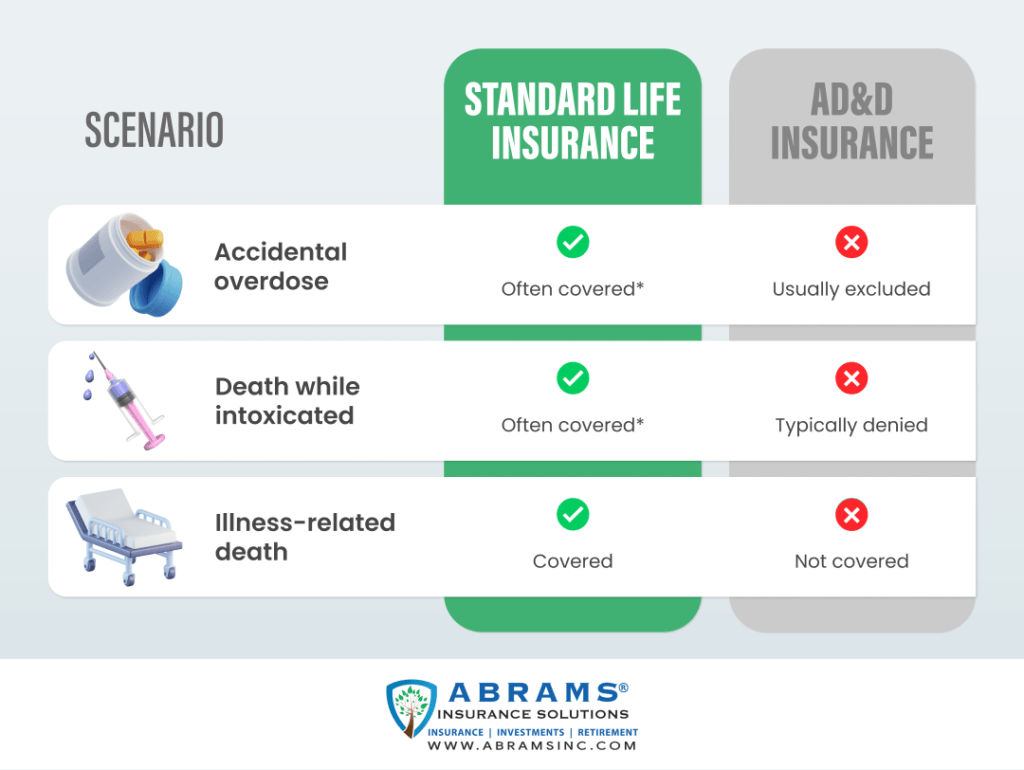

Is an Overdose Considered an Accidental Death?

Short Answer:

In most cases, a drug overdose is not considered an accidental death under Accidental Death & Dismemberment (AD&D) policies. However, it may still be covered under a standard life insurance policy, depending on policy terms and timing.

This is one of the most complex questions in the industry. To understand the answer, we have to distinguish between a standard life insurance policy and an accidental death (AD&D) policy.

Standard Life Insurance

If you have a traditional Term or Whole Life policy that has passed the two-year contestability period, the policy will generally pay out for a drug overdose, provided the application was truthful. If the overdose happens within the first two years, the company will investigate to ensure the drug use wasn’t hidden during the application process.

Accidental Death & Dismemberment (AD&D)

Here’s where things can get a bit confusing. A lot of folks wonder if an overdose is considered an accidental death by an AD&D (Accidental Death & Dismemberment) insurance company.

Here’s the deal: Most AD&D policies specifically exclude deaths that happen when the person is “under the influence” of drugs that weren’t prescribed. So, while a regular life insurance policy might pay out if an overdose occurs, an AD&D policy probably won’t.

Life Insurance for Alcoholics: A Comparative Look

While our focus is on opiates, many applicants struggle with poly-substance use. Life insurance for alcoholics follows a similar underwriting path but often carries different medical markers. Underwriters will look specifically at Liver Function Tests (LFTs) and Carbohydrate-Deficient Transferrin (CDT) levels in your blood work.

Recovery from alcohol addiction is often viewed slightly more leniently than opiate addiction by some carriers, provided there is no evidence of cirrhosis or significant organ damage. However, the same 2-to-5-year sobriety rules generally apply for the best rates.

The Pitfalls of Accidental Death Insurance

As an industry veteran, I see many families turn to Accidental Death insurance because it is cheap and easy to get. However, you must read the fine print.

Important Compliance Note: For an Accidental Death policy to pay out, the death must be a result of a literal accident. Most policies explicitly state that if the insured is under the influence of drugs or alcohol, even if the drug use didn’t “cause” the accident (like a car crash), the claim can be legally denied.

If you are seeking coverage specifically because you are worried about the risks associated with addiction, AD&D is likely not the right tool for you. A small Guaranteed Issue policy is often a more reliable “safety net.”

What to Do If You Need Life Insurance with an Opioid History

If you have a history of opioid or drug addiction, the most important thing to understand is that life insurance eligibility depends on timing, documentation, and carrier selection. The steps below reflect how insurers actually evaluate risk and how applicants in recovery can approach the process strategically.

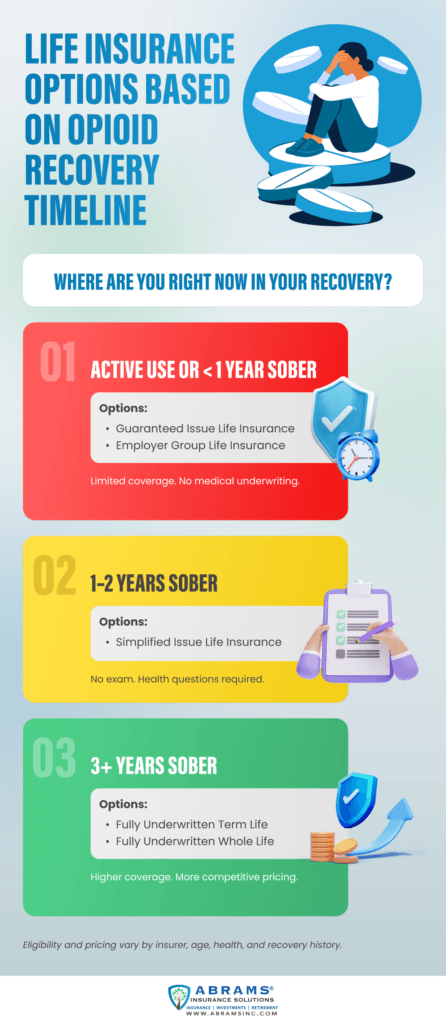

Step 1: Identify Where You Are Right Now

Start by matching your current situation to the coverage options insurers typically consider.

- Active use or very early recovery (under 1 year sober):

At this stage, most traditional life insurance policies are not available. The most realistic options are Guaranteed Issue life insurance or employer-sponsored group life insurance, both of which offer limited coverage without medical underwriting. These policies are often used to address immediate concerns such as final expenses. - 1–2 years of documented sobriety:

Some insurers may consider Simplified Issue life insurance, which does not require a medical exam but does involve health questions. Approval and pricing vary widely at this stage and depend on relapse history, treatment participation, and overall stability. - 3 or more years of sustained recovery:

This is typically when fully underwritten term or whole life insurance becomes viable. These policies offer higher coverage limits and more competitive pricing, assuming no significant secondary health complications related to past substance use.

If you are unsure where you fall, starting with modest coverage can provide short-term protection while preserving the ability to apply for better options later.

Step 2: Apply Strategically, Not Hastily

Once you identify the appropriate policy category, how you apply matters.

- Provide Accurate and Complete Information

Life insurance companies verify applications using medical records, prescription databases, and prior insurance history. Consistent, accurate disclosures help avoid delays, declines, or future claim issues. - Work with an Independent Agent

Independent agents can compare underwriting guidelines across multiple insurers and identify companies that are more receptive to applicants with a history of addiction or recovery. This reduces the risk of unnecessary declines. - Offer Context When Helpful

In some cases, a brief written explanation outlining your recovery timeline, treatment participation, and current lifestyle stability can help underwriters better understand your risk profile. This is especially relevant for applicants in early or mid-stage recovery. - Consider Timing as Part of the Strategy

Waiting to reach additional sobriety milestones can significantly expand eligibility and improve pricing. When waiting is not practical, limited coverage can still serve as a temporary safety net.

Step 3: Revisit Coverage as Recovery Progresses

Life insurance is not a one-time decision. As recovery continues and health remains stable, many policyholders choose to reapply for increased coverage or better rates. Some policies also allow for future reviews or replacements without having to start from scratch.

The goal is not perfection or immediate approval for the largest policy possible. The goal is responsible, phased protection that evolves as your circumstances improve.

Quick Takeaway

People with a history of opioid addiction can often qualify for life insurance, especially after documented recovery. The right approach depends on sobriety duration, medical stability, and applying with carriers that understand recovery-based underwriting.

FAQs

1. How do insurance companies know if I used drugs in the past?

Carriers use several tools: the MIB (Medical Information Bureau), which tracks previous insurance applications; Pharmacy Benefit Managers (PBMs), which show every prescription filled in your name; and Medical Records from your primary care physician or ER visits.

2. Does being on Suboxone or Methadone count as “sober”?

In the eyes of most life insurance underwriters, participation in Medication-Assisted Treatment (MAT) is often viewed as ongoing treatment rather than completed recovery. This does not automatically disqualify an applicant, but it can affect eligibility or pricing depending on the insurer, sobriety duration, and overall health stability.

3. Will my life insurance pay out if I relapse?

If you have a standard policy and you have passed the two-year contestability period, yes. Life insurance is designed to cover deaths regardless of the cause (with very few exceptions, like acts of war). The key is that you were honest on the initial application.

4. Is life insurance for drug addicts more expensive?

Generally, yes. If you are in early recovery, you may be charged a “Flat Extra”, which is an additional fee per $1,000 of coverage. These fees are charged to offset the increased risk of a life insurance claim for a drug overdose.

5. Can I get life insurance for my child who is struggling with addiction?

You can, but you must have “insurable interest,” and the child (even if an adult) must usually sign the application and consent to a medical background check, unless it is a Guaranteed Issue policy with low coverage limits.

6. What happens if the death is ruled an “accidental overdose”?

For a standard life policy, the payout is a death claim. For an AD&D policy, it is frequently denied under the “illegal act” or “substance exclusion” clauses in the policy’s fine print.

Conclusion: Taking the Next Step

Securing life insurance with a history of opiate addiction isn’t about finding a “loophole”. It’s about finding the right timing and the right carrier. Your past does not have to dictate your family’s financial future. While rates may be higher initially, many policies allow you to apply for a “rate reduction” after several more years of documented health and sobriety.

The most important thing you can do today is to get some level of protection in place, even if it’s a small policy, and build from there. So give us a call at 858-703-6178 today. There is never any obligation to buy.

Bottom line: Life insurance for drug addicts is possible, especially after documented recovery, when applications are timed correctly and matched with carriers experienced in recovery-based underwriting.

14 Comments

Louis j Cennamo

Need a quote, I am prescribed Opioid and Depression meds. If you can help please reply. I'm ready now.

Chris Abrams

Bennett sent you an email. There should be some options once we get a few more details from you. Please reply to his email and we'll help you out.

Cynthia Campbell

Im prescribed Suboxone and I keep getting turned down for life insurance. I need help finding a life insurance

Chris Abrams

We have some options that may work for you, but I need some more details such as your age, state and how much coverage you are looking for. I'll email you or feel free to contact me when you have time.

Zach Zirkle

Hello,

I am prescribed suboxone and am looking for term life insurance.

Chris Abrams

We have a few options that you can get now, which include Value 20 Term (https://abramsinc.com/ema-value-20-term-life-insurance/), Guaranteed Issue (https://abramsinc.com/guaranteed-issue-life-insurance-complete-guide/), and Accidental Death (https://abramsinc.com/assurity-accidental-death-insurance-plus-review/). Value 20 and accidental death offer an online application on the respective pages linked. Traditional term life companies will want to see 5 years of no issues after being off the medications. You can use the options above as temporary coverage until we can get you traditional coverage. If you have any questions, please reach out to us by phone or contact form for additional help.

Bridgette Valle

I'm prescribed methadone I'm looking for life insurance or anything to make sure my babies are taken care and I'm covered

Chris Abrams

Hi Bridgette: You can get accidental death insurance which will cover death from any accident. Accidents are one of the leading causes of death for people under 45. You can check rates and apply online here: https://quickstart.assurity.com/Abrams Guaranteed issue policies may be an issue as well, but it will depend on your age and state to know what is available for you. Please reach out at info@abramsinc.com with your state and date of birth and I will see what other options are available for you.

Heidi Allen

I am prescribed suboxone & im wanting life insurance. Plesase help

Chris Abrams

There might be options for you, but I'll need to know the state you live in, date of birth and details of any other health issues? These details can be emailed to info@abramsinc.com.

Mystephanie Finney

Hello! I was prescribed suboxone, it wasn’t even for opiates. It was to stop using Kratom, a plant. I’ve never had an issue finding life insurance before and I regret the decision to use suboxone. Please help me find coverage.

Chris Abrams

I sent you an email to collect some more details so I can see what options will be available for you.

Patrick Connolly

Chris, I am on Suboxone and need term life insurance. Could you help me?

My email is connolly_patrick@comcast.net

Thank you!

Chris Abrams

Bennett from my team already reached out to you.